Why USDC Remittance Infrastructure Matters Now

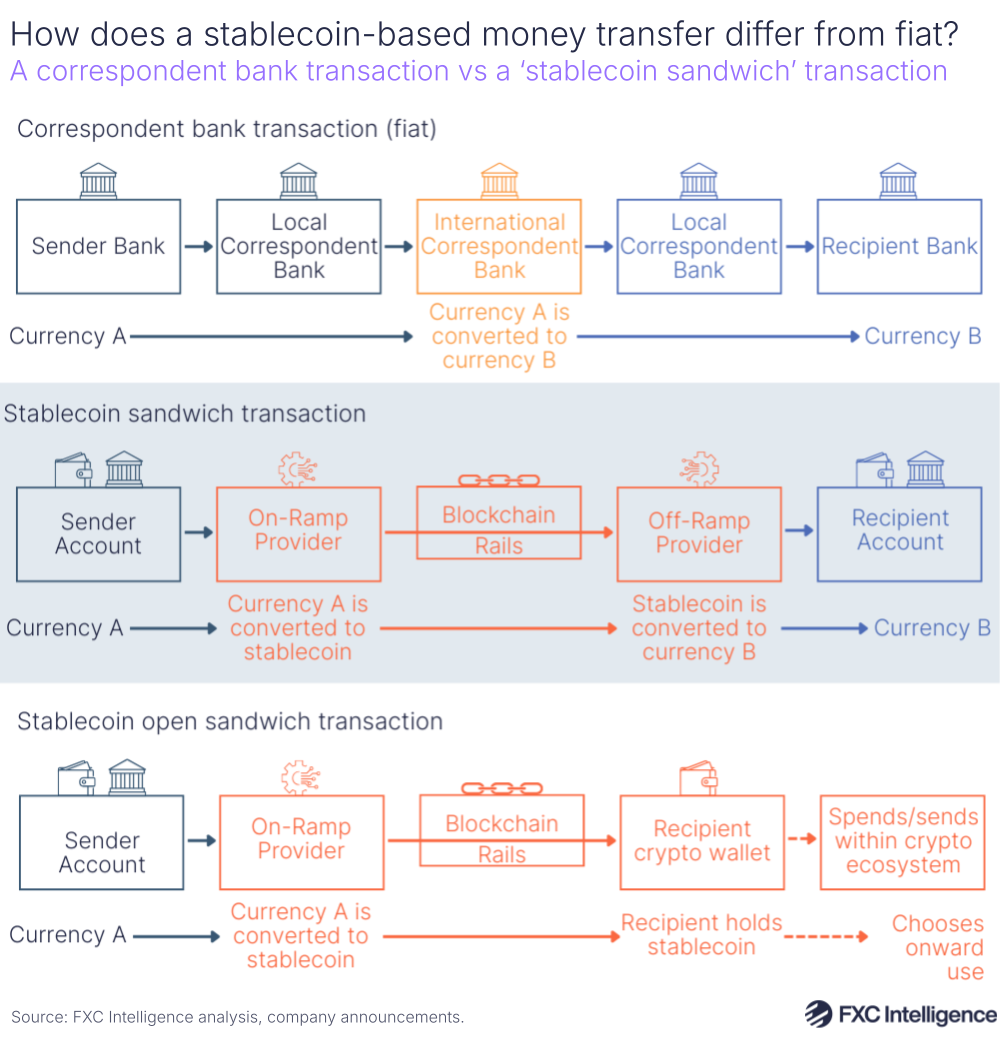

Traditional cross-border payment rails are facing an existential efficiency crisis. For finance professionals managing payroll, vendor settlements, or personal remittances, the current infrastructure imposes unacceptable friction. The legacy banking system—reliant on correspondent networks and SWIFT messaging—often takes three to five days to settle, with fees that erode the value of the transfer before it even reaches the recipient.

The economic urgency is clearest in high-volume corridors like the US-Mexico route. According to Mizuho research cited by Polygon, remittance fees via stablecoin rails in this corridor have dropped below 1%. This stands in stark contrast to the 5% to 7% average cost of traditional money transfer operators. For a migrant worker sending $500 home, that difference is not just a margin; it is a significant portion of their income preserved. This cost reduction is not theoretical; it is a measurable advantage that USDC infrastructure delivers immediately.

Speed is the other half of the equation. While banks operate on business days and cut off at specific hours, USDC settles in minutes, 24/7. This near-instant liquidity allows businesses to manage cash flow with precision and individuals to access funds when emergencies arise. The shift is no longer about technological novelty; it is about adopting a payment layer that matches the speed of modern commerce.

Selecting the Right USDC Remittance Partners

Building a remittance infrastructure requires choosing between direct integration with Circle and utilizing API aggregators like Crossmint or Stripe. The decision hinges on balancing compliance overhead, integration speed, and transaction costs. Direct integration offers maximum control but demands significant engineering resources, while aggregators provide faster time-to-market with built-in compliance frameworks.

Direct Integration with Circle

Integrating directly with Circle’s infrastructure allows you to manage USDC issuance, redemption, and transfers natively. This approach is ideal for institutions with robust compliance teams and the engineering capacity to handle blockchain interactions. Circle provides direct access to its reserves and regulatory reporting, ensuring transparency. However, this path requires building and maintaining your own wallet infrastructure and liquidity management systems.

API Aggregators: Crossmint and Stripe

Aggregators like Crossmint and Stripe abstract away much of the complexity. Crossmint offers specialized stablecoin remittance APIs designed for fintechs and money transfer companies, enabling cross-border payments using USDC and USDT with minimal code. Stripe’s stablecoin infrastructure integrates USDC into its existing payment rails, leveraging its strong regulatory ties and mainstream financial integrations. These platforms reduce compliance burden and accelerate launch timelines, though they may introduce higher per-transaction fees and less granular control over the underlying blockchain state.

| Provider | Integration Speed | Compliance Burden | Cost Structure | Control Level |

|---|---|---|---|---|

| Circle (Direct) | Slow (Months) | High | Variable (Gas + Network) | Full |

| Crossmint | Fast (Weeks) | Medium | API Fees + Network | Partial |

| Stripe | Fast (Weeks) | Low | Standard Stripe Fees | Low |

Evaluating Compliance and Speed

When selecting a partner, prioritize providers with clear regulatory standing. Circle’s USDC is backed by cash and short-dated US Treasuries, with regular attestation reports. Stripe and Crossmint both emphasize compliance-first designs, but their specific KYC/AML requirements vary. For speed, API aggregators typically offer SDKs and pre-built modules, reducing development time by 60-80% compared to direct integration. Consider your team’s capacity: if engineering resources are limited, an aggregator is the pragmatic choice. If you require full custody and audit trails, direct integration is necessary.

As an Amazon Associate, we may earn from qualifying purchases.

Executing the Cross-Border Settlement Flow

Building a USDC remittance infrastructure requires a precise sequence of operations to ensure funds move securely from the sender’s fiat on-ramp to the receiver’s local off-ramp. Unlike traditional banking rails that rely on correspondent accounts and manual reconciliation, this workflow leverages smart contracts and stablecoin networks to achieve near-instant settlement. The process is divided into five distinct phases, each requiring specific technical and compliance checks.

The journey begins when the sender deposits fiat currency (USD, EUR, etc.) into a regulated on-ramp provider. This provider must be licensed in the sender’s jurisdiction and integrated with your core ledger. Upon confirmation of the fiat deposit, the provider mints or releases an equivalent amount of USDC. This step is critical for compliance; ensure your system captures the sender’s identity (KYC) and transaction purpose before any digital assets are generated. The on-ramp provider typically charges a fee ranging from 0.5% to 1.5%, which should be clearly disclosed to the user.

Once USDC is in the sender’s wallet or your custodial pool, it must be routed to the recipient’s network. For most remittance corridors, Polygon or Solana are preferred over Ethereum Mainnet due to lower gas fees and faster finality. Your infrastructure should automatically select the optimal chain based on the destination country’s liquidity and regulatory environment. Circle’s documentation confirms that USDC is available on over 20 blockchains, but sticking to a primary chain for a specific corridor reduces complexity and counterparty risk. Ensure your system monitors gas prices to execute transactions during low-congestion windows, further reducing costs.

The actual transfer is executed via a smart contract call. If you are using a custodial model, your backend signs the transaction using a multi-signature wallet. If you are integrating with non-custodial wallets, you may use account abstraction or social login solutions to simplify the user experience. The transaction includes the recipient’s wallet address and the amount. At this stage, your system should generate a unique transaction ID that links the on-chain hash to your internal ledger. This linkage is essential for dispute resolution and audit trails. Circle’s transparency reports show that USDC transactions on supported networks typically settle in under 2 seconds.

After broadcasting the transaction, your system must wait for block confirmation. The number of confirmations required depends on the network’s security model; for Polygon, 12-20 confirmations are standard for high-value transfers. During this window, the status in your dashboard should reflect "Processing." Do not notify the recipient of completion until the on-chain state is irreversible. This step prevents double-spending attacks and ensures that the funds are truly settled before initiating the off-ramp process. Implementing a webhook listener for on-chain events allows your backend to update the ledger automatically without polling.

The final step is converting the USDC into local currency for the recipient. This is done through a regulated off-ramp partner or a local liquidity provider. The off-ramp receives the USDC from your system, verifies the on-chain confirmation, and disburses local fiat via bank transfer, mobile money, or cash pickup. The recipient’s bank or payout provider typically charges a fee, which varies by country. Ensure your system has real-time exchange rate integration to lock in the rate at the moment of off-ramp initiation, protecting both you and the recipient from volatility during the conversion window. The entire flow, from fiat deposit to local cash-out, should take less than 5 minutes for most major corridors.

Critical Implementation Considerations

When building this flow, prioritize the integrity of the ledger over speed. A mismatch between your internal database and the on-chain state can lead to significant financial loss. Implement a reconciliation job that runs every 5 minutes to compare your ledger balances against the blockchain state. Additionally, ensure your off-ramp partners have sufficient liquidity in the recipient’s currency to avoid delays. Finally, always comply with local regulations regarding virtual asset service providers (VASPs), including the FATF Travel Rule, which requires you to share sender and recipient information with the next VASP in the chain.

Managing Compliance and Regulatory Risk

Building a USDC Remittance Infrastructure works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Common Mistakes in USDC Remittance Setup

Building a USDC remittance pipeline is straightforward in theory but fragile in practice. The difference between a smooth user experience and a failed transaction often comes down to three specific operational choices: network selection, liquidity management, and on-ramp integration. Avoiding these pitfalls requires prioritizing speed and cost efficiency over convenience.

Choosing the Wrong Network

Many teams default to Ethereum Mainnet for USDC transfers because it is the most recognized chain. This is a critical error for remittance. Transaction fees on Ethereum can range from $5 to $20 or more, depending on network congestion, while settlement times vary unpredictably. For cross-border payments where margins are thin, these costs erase profitability.

Instead, select Layer 2 solutions or high-throughput chains like Polygon or Solana. Polygon, for instance, offers near-instant finality with fees typically under $0.01. Circle supports USDC on these networks with the same 1:1 USD peg and regulatory compliance as Ethereum. The technical integration is nearly identical, but the unit economics are drastically different. Always benchmark the average transfer cost against your target margin before finalizing the network.

Underestimating Liquidity Requirements

A common mistake is assuming that holding USDC in a hot wallet is sufficient for processing payouts. When a user requests a withdrawal, you need immediate liquidity in the destination currency (fiat or local stablecoin) to settle the transaction. If your partner exchange or liquidity provider has a delay or cap, your users experience failed payouts.

Establish pre-funded liquidity lines with multiple providers. Do not rely on a single on-ramp partner for both inbound and outbound flows. If one partner experiences downtime or rate limits, your entire remittance service halts. Diversify your liquidity sources to ensure that a bottleneck in one channel does not stop the entire pipeline.

Ignoring User Experience Friction

The final mistake is treating crypto wallets like traditional bank accounts. Users do not want to manage private keys, gas fees, or network selection. If your interface requires them to understand what a "gas fee" is or which network to select, you have lost the adoption advantage.

Abstract the complexity. Use account abstraction or sponsored transactions where possible so users never see a gas fee. Ensure your UI clearly displays the expected arrival time and total cost upfront. The goal is to make USDC feel as invisible as a credit card transaction, not as a complex crypto operation.

Final Checklist for Launching USDC Remittances

Before you go live, treat your infrastructure like a high-stakes audit. You are moving value across borders, so the margin for error is zero. This checklist ensures your USDC remittance rails are secure, compliant, and ready for production traffic.

Once these steps are verified, your infrastructure is ready. You are now positioned to offer faster, cheaper remittances than traditional banking rails.

No comments yet. Be the first to share your thoughts!