Why USDC leads cross-border settlement

The cross-border payments industry is massive, reaching $159 trillion in 2022, yet the infrastructure for moving that value remains fragmented and slow. USDC has emerged as the dominant stablecoin for remittances because it solves the friction that plagues traditional banking corridors. Unlike legacy systems that route money through multiple correspondent banks, USDC allows value to move directly between digital wallets on the blockchain. This structural advantage reduces both the time and the cost of sending money across borders.

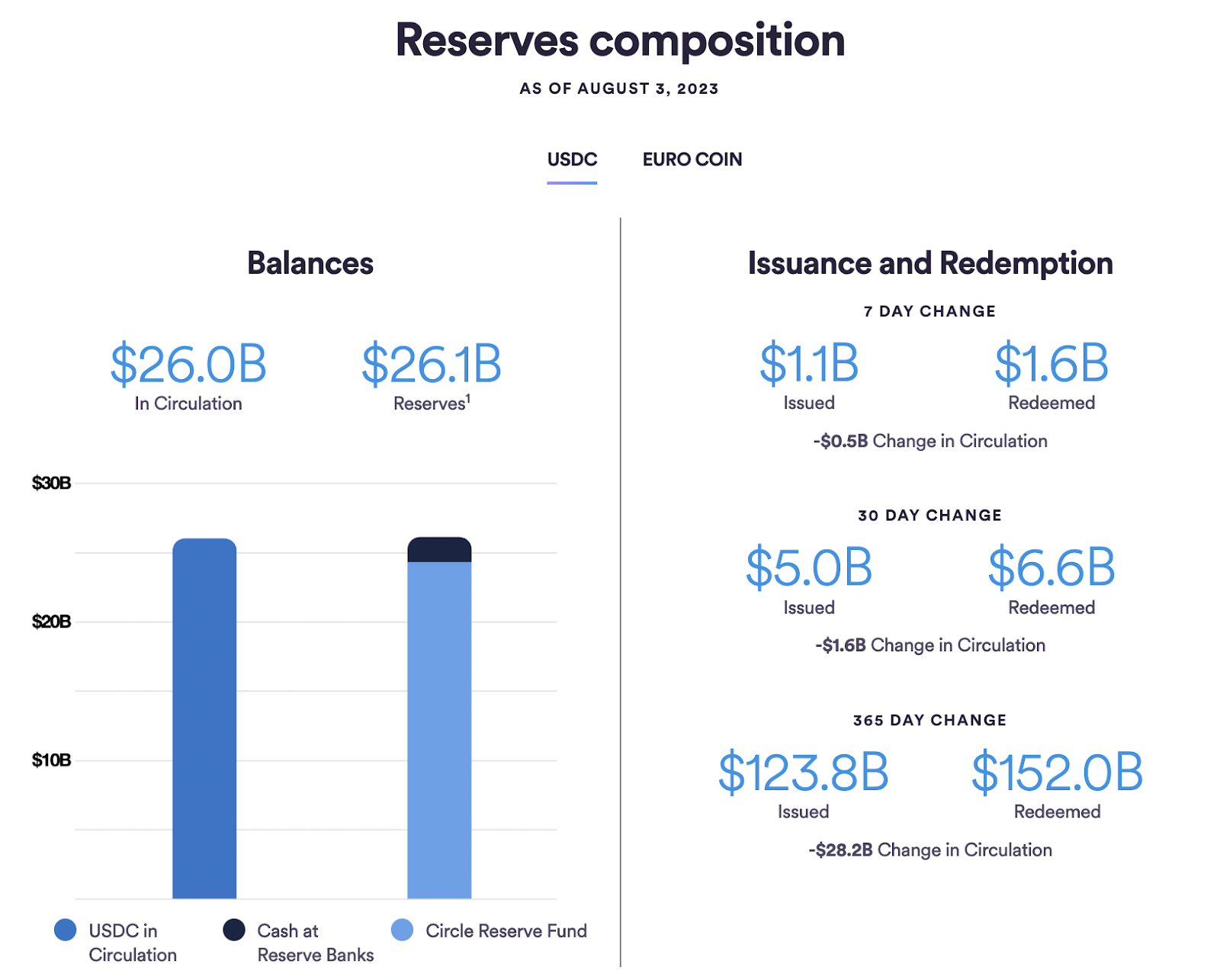

Regulatory clarity is the bedrock of this dominance. USDC is fully collateralized by U.S. dollars and short-term U.S. Treasuries, and it operates under strict regulatory oversight. This transparency is critical for high-stakes financial decisions where trust in the underlying asset is non-negotiable. While other stablecoins may offer similar price stability, they often lack the same level of regulatory scrutiny and reserve transparency. For remittance providers and users alike, this distinction reduces counterparty risk and ensures that the digital dollar on-chain truly represents a dollar in the bank.

Liquidity and infrastructure readiness further solidify USDC's position. The network is supported by deep liquidity pools on major exchanges and a growing ecosystem of regulated on-ramp and off-ramp providers. This means that converting USDC to local fiat currencies in emerging markets is faster and more reliable than with less established tokens. As the industry continues to grow at a 5% annual pace, the institutions building the rails are choosing USDC for its compliance-first approach. This network effect creates a moat that is difficult for competitors to breach, making USDC the pragmatic choice for 2026 and beyond.

USDC Remittance vs. Traditional Rails

Moving money across borders has long been defined by a trade-off: speed or cost, rarely both. Traditional methods like SWIFT and money transfer operators (MTOs) have built their business models on opacity and friction. USDC remittance flips this dynamic by leveraging blockchain infrastructure to settle value in minutes rather than days, often at a fraction of the cost.

The difference is stark. A typical cross-border transfer via SWIFT can take two to five business days, involving multiple intermediary banks that each take a cut. MTOs like Western Union charge significant percentage-based fees, particularly for smaller amounts. In contrast, USDC transactions settle on-chain in seconds to minutes, regardless of the destination, with fees that remain consistent and transparent.

Cost and Speed Comparison

The following comparison highlights the operational differences between USDC and traditional rails. While MTOs offer physical cash pickup convenience, their cost structure penalizes the sender. USDC requires digital literacy and access, but offers superior efficiency for those who can use the infrastructure.

| Method | Settlement Time | Avg. Cost | Accessibility |

|---|---|---|---|

| USDC (On-Chain) | Seconds to Minutes | <$0.01 to $0.50 | Digital wallet required |

| SWIFT Wire | 1–5 Business Days | $15–$50+ | Bank account required |

| Western Union | Minutes (Cash Pickup) | 3–10% of amount | Physical agent locations |

The Hidden Costs of Traditional Rails

Traditional banking rails are not just slow; they are expensive. The World Bank’s Global Findex data consistently shows that the average cost of sending $200 remains above 6%, far exceeding the UN Sustainable Development Goal target of 3%. Intermediary banks often deduct fees from the principal amount, meaning the recipient gets less than what was sent. USDC eliminates these middlemen. By moving directly from sender to receiver on a public ledger, you avoid the markup layers that inflate traditional remittance costs.

Accessibility and Infrastructure

While USDC offers superior speed and cost, accessibility remains a nuanced factor. Traditional MTOs have extensive physical networks, allowing unbanked populations to receive cash. USDC requires a smartphone and internet connection. However, the gap is closing as digital wallets become more user-friendly and local exchange rates stabilize. For individuals with digital access, USDC provides a significantly more efficient alternative to legacy systems.

When to Use Which

USDC remittance is ideal for recurring payments, high-value transfers, and situations where time sensitivity is critical. Traditional rails may still be preferable for recipients who lack digital infrastructure or require immediate cash access without a bank account. Understanding these trade-offs allows senders to choose the right tool for the job, optimizing both cost and convenience.

As an Amazon Associate, we may earn from qualifying purchases.

Infrastructure upgrades driving volume

The recent surge in cross-border payments is no longer just about demand; it is about capacity. In January 2026, adjusted stablecoin transfer volume hit a record $8 trillion, with the vast majority of that growth driven by USDC on Base [[src-serp-7]]. This isn't a temporary spike. It is the result of specific technical upgrades that have removed the friction traditionally associated with USDC remittance analysis and execution.

For years, cross-border transfers were bottlenecked by legacy banking rails. USDC changed this by allowing money to move directly between digital wallets, bypassing the need for multiple correspondent banks [[src-serp-1]]. However, the real breakthrough came with the scaling of Base. As a Layer 2 solution built on Ethereum, Base offers significantly lower transaction costs and higher throughput. This infrastructure shift means that sending $50 or $50,000 costs roughly the same in fees, making USDC viable for both micro-transfers and institutional settlement.

The network effect is now self-reinforcing. More developers building on Base means more user-friendly apps, which drives more volume, which justifies further infrastructure investment. This cycle has turned USDC from a simple payment rail into a foundational settlement layer for global finance.

The integration of USDC into broader settlement networks, such as the recent partnership between Nium and Circle, further solidifies this infrastructure. These partnerships are not just about adding liquidity; they are about embedding USDC into the core plumbing of remittance providers, ensuring that the technical upgrades we see today translate into reliable, low-cost transfers for users tomorrow.

Strategic Tools for Global Settlement

Executing USDC remittances efficiently requires moving beyond raw blockchain transactions to integrated platforms that handle compliance and liquidity. Businesses and individuals rely on specialized infrastructure to bridge the gap between digital assets and local fiat currencies, ensuring funds arrive quickly and legally.

Platform Integration and Compliance

Platforms like Due have emerged to streamline these cross-border payments by leveraging stablecoins for speed and lower fees. By utilizing USDC, these services bypass traditional correspondent banking networks, which often introduce delays and opaque charges. The result is a transparent, audit-ready ledger that simplifies accounting for high-volume senders.

Regional Settlement: The Félix Model

For specific corridors, such as transfers from the US to Mexico, infrastructure providers like Félix partner directly with Circle to optimize the flow of value. Félix uses USDC to reduce the cost of transferring customer funds, offering a regulated alternative to cash-based remittance services. This approach ensures that the underlying asset remains fully collateralized while the settlement layer handles local fiat payouts.

Key questions on safety and ownership

When moving money across borders, you need to know exactly who holds the funds. USDC is issued by Circle, not the U.S. government. It is fully backed by cash and short-term U.S. Treasuries, meaning every token is redeemable for a dollar at par. This structure provides a clear audit trail for your USDC remittance strategy, distinguishing it from unregulated offshore assets.

The biggest concern for many users is the difference between USDC and USDT. USDC is generally considered safer because it is fully collateralized and subject to U.S. regulatory oversight. Tether (USDT), by contrast, has historically used a mix of reserves and commercial paper, making its backing less transparent. For high-stakes transfers, the regulatory clarity of USDC reduces counterparty risk.

No comments yet. Be the first to share your thoughts!