USDC remittance analysis: real-world limits to account for

USDC remittance analysis reveals a clear trade-off between speed and regulatory overhead. While the technology offers near-instant settlement, the actual friction lies in compliance and liquidity routing. Unlike traditional wire transfers that move through correspondent banks, USDC transactions settle on-chain, but the on-ramps and off-ramps remain heavily regulated.

The primary constraint is not the blockchain itself, but the fiat gateways. Providers like BCRemit have integrated Circle’s USDC to bypass legacy banking delays, but they must still navigate KYC/AML requirements at both ends. This creates a "last mile" problem where the speed of the blockchain is nullified by the slowness of fiat conversion. For high-volume remitters, this means USDC is an infrastructure layer, not a standalone product.

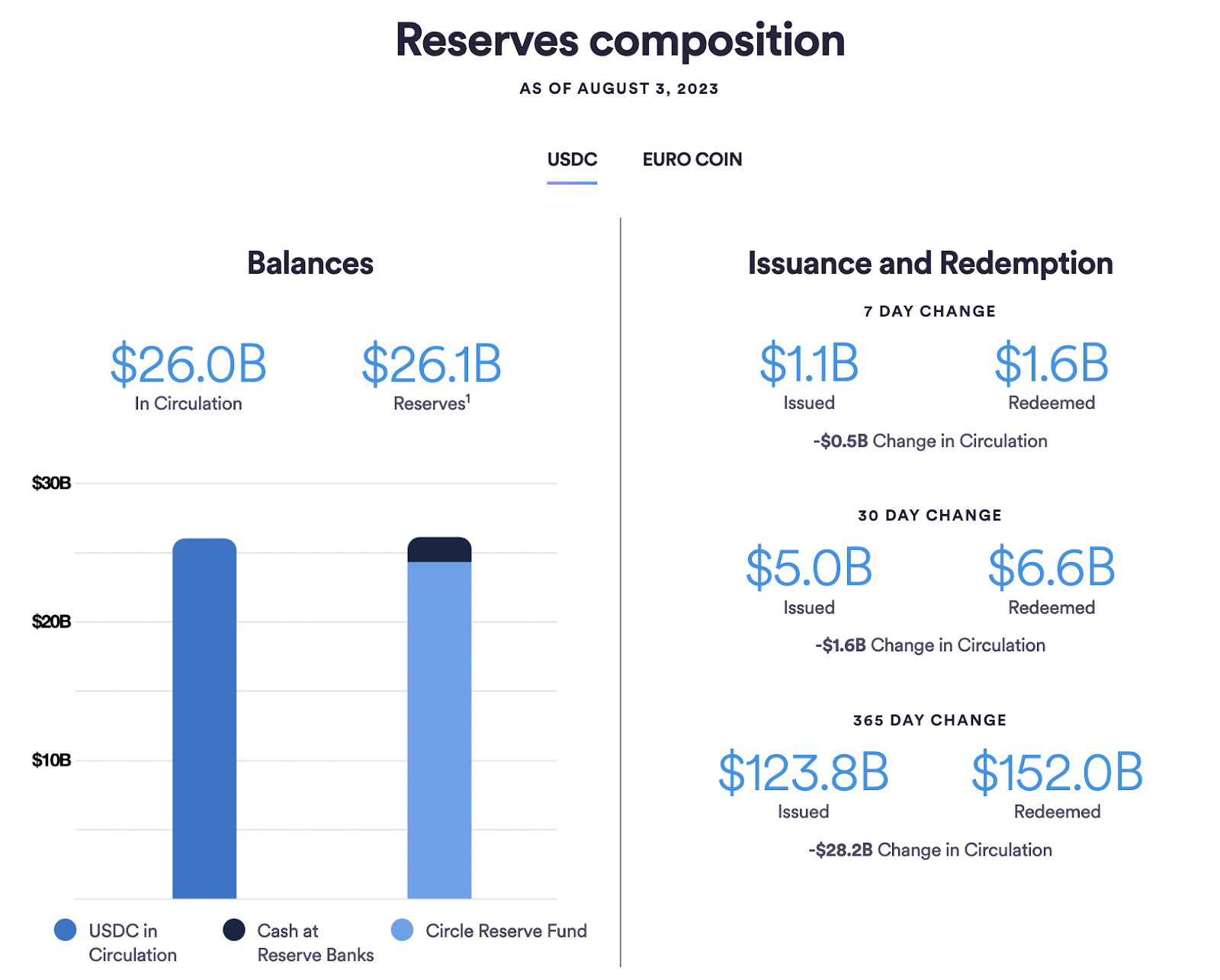

Safety is another critical factor. USDC is not owned by the U.S. government, despite common misconceptions. It is issued by Circle, a private company, and backed by reserves including cash and short-term U.S. Treasuries. While considered a "gold standard" for safety, it is not risk-free. Banking system exposure remains a vulnerability; a systemic failure in U.S. banks could cause a temporary de-peg, as seen during the 2023 SVB collapse. Users must weigh this counterparty risk against the convenience of real-time settlement.

Usdc remittance analysis choices that change the plan

Use this section to make the USDC Remittance Analysis decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

How to Build a USDC Remittance Decision Framework

Choosing a stablecoin for cross-border payments requires balancing speed, cost, and regulatory safety. USDC has emerged as a primary settlement layer for remittances, but it is not a monolithic solution. The right strategy depends on your specific volume, destination corridors, and risk tolerance. This framework breaks down the essential checks for integrating USDC into your remittance infrastructure.

USDC is fully backed by U.S. dollars and short-dated U.S. Treasuries, but it is not issued by the U.S. government. Its safety relies on Circle’s reserve management. A critical risk is banking system exposure; if a portion of reserves is held in traditional banks, a systemic failure could cause a temporary de-peg, as seen during the 2023 SVB collapse. Always review Circle’s monthly attestation reports to ensure reserves are fully liquid and segregated.

Not all corridors support efficient USDC settlement. Partners like BCRemit have successfully leveraged USDC to make remittances faster and cheaper, but this requires deep local liquidity pools. Before integrating, verify that your payout partners can convert USDC to local fiat instantly at competitive rates. High slippage or delayed conversions in emerging markets can erase the cost advantages of blockchain settlement.

USDC exists on multiple blockchains, each with different fee structures and finality speeds. For high-volume remittances, layer-2 networks like Arbitrum or Optimism often offer near-zero fees and sub-second finality compared to Ethereum mainnet. However, you must ensure your recipient’s wallet or exchange supports the chosen network. Mismatched networks can lead to lost funds or significant withdrawal fees for the end-user.

Remittance providers operate under strict anti-money laundering (AML) and know-your-customer (KYC) regulations. USDC’s compliance-friendly design makes it easier to integrate with regulated financial services, but it also means transactions can be frozen if addresses are flagged. Build robust screening tools into your workflow to prevent compliance breaches. Understand the local regulatory stance on stablecoins in both your origin and destination countries to avoid future operational disruptions.

As an Amazon Associate, we may earn from qualifying purchases.

Spotting Weak Options in USDC Remittance

Real-time settlement sounds ideal, but the infrastructure behind it varies wildly. Many providers market speed while hiding high FX spreads or opaque reserve structures. When evaluating USDC remittance channels, look past the "instant" claims and check the actual settlement path. If the provider doesn't publish their reserve attestation or routing partners, treat the speed claim with skepticism.

Common Mistakes to Avoid

Assuming USDC is Government-Backed USDC is not issued by the U.S. government. It is a private stablecoin fully backed by U.S. dollars and short-term Treasuries. Confusing this distinction can lead to regulatory surprises if your provider faces compliance issues. Always verify the issuer’s regulatory status in your jurisdiction.

Ignoring Reserve Transparency Not all stablecoins are created equal. USDC’s monthly attestations are a baseline, but weak options may use commingled funds or unverified bank deposits. Check if the provider discloses their custodial partners. If they don’t, you’re taking on counterparty risk that isn’t visible in the transfer fee.

Overlooking De-peg Risks While USDC is considered robust, it is not risk-free. During the 2023 SVB collapse, USDC briefly de-pegged due to banking exposure. For remittances, this means temporary delays or reduced liquidity during systemic stress. Ensure your provider has a clear recovery plan or alternative liquidity sources.

The Bottom Line

Speed means nothing if the settlement fails. Prioritize providers with transparent reserves, clear regulatory compliance, and proven liquidity during market stress. Avoid any option that can’t answer these questions with public documentation.

USDC Remittance Questions Answered

Before integrating USDC into your cross-border strategy, it is important to address the practical risks and structural realities of the asset. While USDC offers speed and transparency, it operates differently from traditional fiat rails.

Is USDC in danger?

USDC is not risk-free, despite being considered a "gold standard" for safety among stablecoins. The primary risk stems from its reserve structure. A portion of USDC reserves is held in traditional banking partners. If a systemic failure occurs in the U.S. banking sector, it could cause a temporary "de-peg," similar to the event during the 2023 Silicon Valley Bank collapse. However, Circle has since diversified reserves to mitigate this specific exposure.

Is USDC owned by the U.S. government?

No. USD Coin (USDC) is a private stablecoin issued by Circle, not the U.S. government or the Federal Reserve. It is fully backed by U.S. dollars and short-term U.S. Treasury bonds. While it uses the dollar as its anchor, it is not a digital dollar or a central bank digital currency (CBDC). This distinction matters for regulatory compliance and institutional adoption.

How does USDC compare to traditional remittance costs?

Traditional remittance services involve multiple intermediaries—correspondent banks, clearing houses, and local payout agents—each taking a fee. USDC moves directly between digital wallets on the blockchain. This infrastructure reduces the cost of sending money across borders significantly, often by 50-80% compared to legacy providers like Western Union or MoneyGram, while settling in minutes rather than days.

Is USDC legal for remittances in the U.S.?

Yes, using USDC for remittances is legal in the United States, provided the service provider complies with federal regulations. Companies facilitating these transfers must register as Money Service Businesses (MSBs) with FinCEN and implement robust Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols. The legal framework is established, though regulatory clarity continues to evolve.

No comments yet. Be the first to share your thoughts!