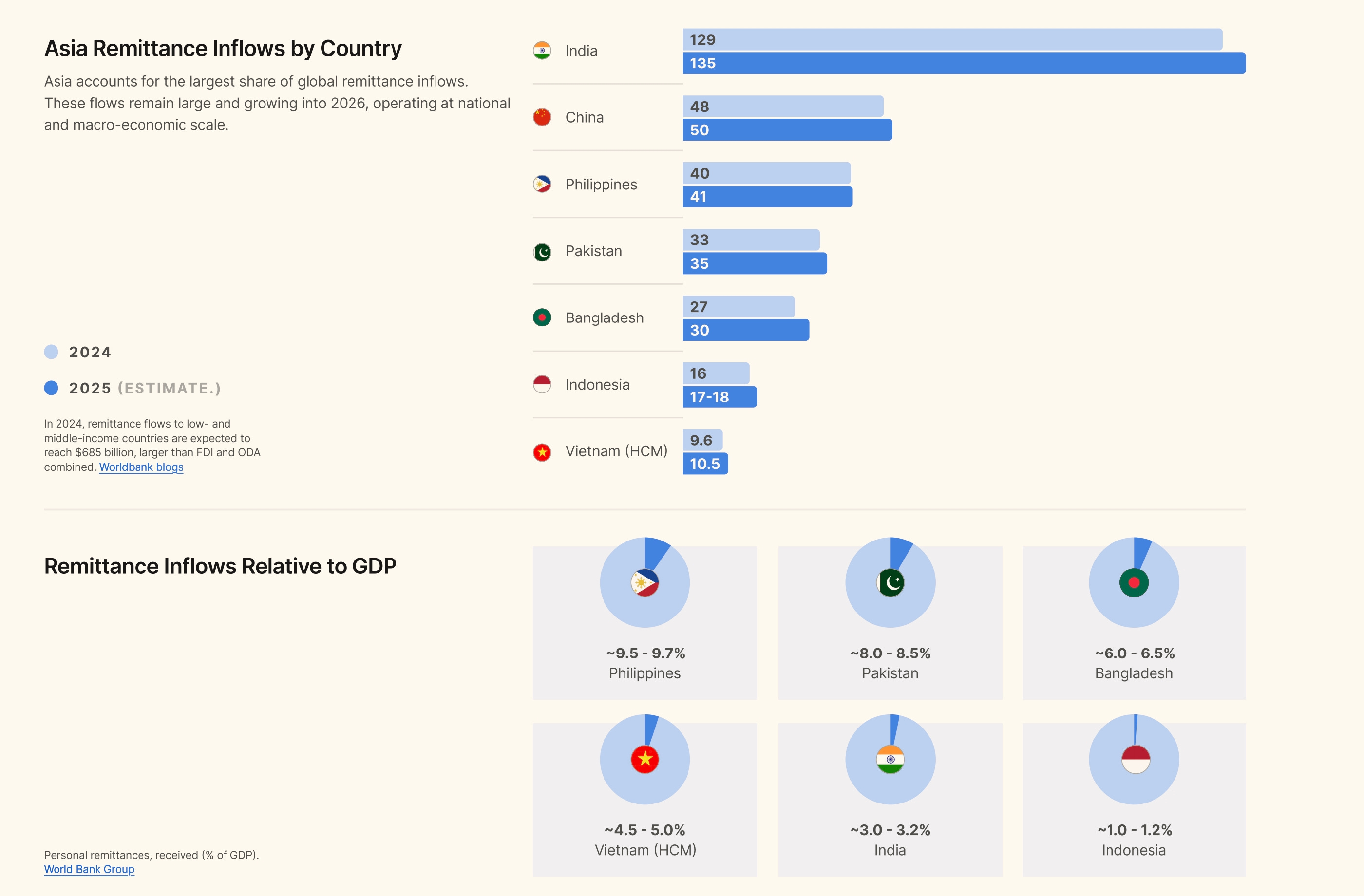

Why USDC reshapes remittance economics

Traditional remittance corridors are defined by friction. Sending money across borders through legacy banking rails often involves a chain of intermediaries, each taking a cut and adding days to the settlement time. For a family relying on funds to cover immediate needs, those delays and hidden fees represent a significant tax on trust. USDC changes this dynamic by offering a direct, on-chain alternative that prioritizes speed and transparency.

The core advantage lies in the settlement architecture. While SWIFT transfers can take three to five business days to clear, USDC transactions settle in minutes, regardless of weekends or holidays. This speed is not just a convenience; it reduces the exposure to currency fluctuation risks that plague multi-day fiat transfers. The recipient gets the exact amount sent, minus minimal network fees, rather than a reduced sum after intermediary deductions.

Cost structures also shift dramatically. According to industry analysis from Stripe, stablecoins like USDC allow businesses and individuals to move value without the steep markup fees associated with traditional wire services. By leveraging the infrastructure of regulated payment platforms, users can access these lower costs without needing to navigate complex crypto exchanges directly. The result is a clearer, more predictable cost basis for every transaction.

To understand the current market context for USDC, it is useful to monitor its price stability and trading volume. A consistent peg to the US dollar is fundamental to its utility in remittances, ensuring that the value sent is the value received.

USDC vs traditional money transfer costs

When sending money across borders, the headline fee is rarely the only cost. Traditional services like Western Union and MoneyGram often bundle transfer fees with unfavorable foreign exchange (FX) spreads, while USDC remittances separate these costs, offering a more transparent pricing model. Understanding this spread is critical for determining the true cost of your transfer.

The Fee Structure Breakdown

Traditional money transfer operators typically charge a flat fee based on the amount sent and the payout method. However, the hidden cost often lies in the exchange rate. If you send $100 to a recipient in a country with a different currency, the service provider may apply a spread of 3-5% on the conversion rate. This means the recipient might only receive the equivalent of $95-$97, even if the transfer fee was low or zero.

In contrast, USDC is pegged 1:1 to the US dollar. When you send USDC, the recipient receives the exact same value, minus only the network gas fees and any exchange fees if they need to convert to local currency. Network fees on stablecoin chains like Solana or Polygon are often fractions of a cent, while Ethereum mainnet fees can range from $1 to $10 depending on network congestion. This structure eliminates the FX spread entirely for the transfer leg.

Side-by-Side Cost Comparison

The table below compares the typical costs for sending $100 to a major remittance corridor (e.g., US to Mexico or Philippines) using traditional services versus USDC on low-fee chains.

| Method | Transfer Fee | FX Spread | Total Cost | Speed |

|---|---|---|---|---|

| Western Union | $4-8 | 3-5% | $7-13 | Minutes |

| MoneyGram | $4-7 | 3-5% | $7-12 | Minutes |

| USDC (Polygon) | <$0.01 | 0% | <$0.01 | Seconds |

| USDC (Solana) | <$0.01 | 0% | <$0.01 | Seconds |

| USDC (Ethereum) | $1-10 | 0% | $1-10 | Minutes |

Real-World Impact

For smaller transfers, the fixed fees of traditional services can consume a significant portion of the sent amount. Sending $50 via Western Union might cost $5 in fees plus a 4% FX spread, totaling $7 in costs (14% of the transfer). The same $50 sent via USDC on Polygon would cost less than a penny in fees, representing a 99.9% reduction in cost.

Even on Ethereum, where gas fees are higher, USDC remains competitive for larger transfers where the FX spread of traditional services would otherwise exceed $10. The key advantage is predictability: with USDC, you know exactly how much the recipient will get before you send it, whereas traditional services often provide an "estimated" exchange rate that can change by the time the money is picked up.

When Traditional Services Still Win

Despite the cost advantages of USDC, traditional services remain dominant in specific scenarios. The primary advantage is accessibility. Recipients can pick up cash at thousands of physical locations without needing a smartphone, internet connection, or crypto wallet. For unbanked populations in rural areas, this physical access point is invaluable.

Additionally, traditional services offer a layer of dispute resolution and customer support that is still evolving in the crypto space. If a transaction is sent to the wrong address, it is often irreversible. Traditional services can sometimes reverse fraudulent transactions or provide recourse for lost funds, a safety net that USDC transfers currently lack.

The Verdict

For tech-savvy users and businesses prioritizing cost efficiency and speed, USDC is the clear winner. The elimination of FX spreads and minimal network fees make it significantly cheaper for most transfer sizes. However, for recipients who lack digital infrastructure or require immediate cash pickup without a bank account, traditional services like Western Union remain the practical choice. The best strategy often involves using both: USDC for regular, cost-sensitive transfers and traditional services for occasional, urgent cash needs.

Infrastructure upgrades driving 2026 adoption

The 2026 remittance landscape is defined by a shift from experimental crypto pilots to institutional-grade infrastructure. The primary driver is the integration of Circle’s Mint, which provides a regulated, compliant layer for issuing and redeeming USDC. This allows remittance providers to move funds on-chain with the same certainty as traditional banking rails, eliminating the historical friction of liquidity gaps and settlement delays.

Beyond issuance, the backbone of this strategy lies in non-custodial wallet technology and specialized stablecoin rails. As noted by Mastercard’s analysis of the future of remittances, platforms like BCRemit and MoneyGram are leveraging non-custodial wallets to bridge the gap between crypto and fiat. These wallets allow users to hold and transfer USDC directly, reducing reliance on third-party custodians and lowering the risk profile for both the provider and the end-user.

This technical maturity is supported by robust compliance frameworks. Fireblocks and similar infrastructure providers now serve over 2,400 organizations, offering the audit trails and regulatory reporting required by financial authorities. For remittance corridors in Latin America and Asia, this means that USDC is no longer just a speculative asset but a functional utility for moving value across borders.

The stability of this infrastructure is reflected in the market. USDC maintains its peg through a reserve model backed by short-duration U.S. Treasuries and cash equivalents, ensuring that the value remains consistent regardless of market volatility. This stability is critical for remittances, where even minor fluctuations can erode the value of the transfer for the recipient.

Real-world case studies in Latin America and Europe

Theoretical cost savings mean little without execution. In Latin America, specifically Colombia, the integration of USDC into existing financial rails is already reshaping how remittances move. Companies like BCRemit have moved beyond pilot programs, leveraging Circle’s infrastructure to offer transfers that are faster and significantly cheaper than traditional wire services [src-serp-1].

For Colombian businesses, the benefit extends beyond simple transfer fees. By pairing virtual USD accounts with near-instant USDC on-chain transfers, SMEs gain faster access to working capital while reducing exposure to peso volatility [src-serp-3]. This dual advantage—speed and hedging—is difficult to replicate with legacy banking corridors.

The broader industry is following this lead. Mastercard, in collaboration with Stellar, has developed non-custodial wallets that bridge crypto and fiat using USDC to accelerate settlement times [src-serp-5]. While Europe’s regulatory landscape remains distinct, the Latin American adoption curve provides a clear blueprint: USDC is not just a speculative asset, but a functional settlement layer for high-volume corridors.

In Europe, the strategy shifts from accessibility to compliance. European fintechs are increasingly using USDC to settle cross-border B2B payments, bypassing the SWIFT network’s latency. This is particularly relevant for the Eurozone, where intra-EU transfers are seamless but global ones remain expensive. By holding USDC on-chain, European businesses can settle international debts instantly, avoiding the multi-day float that ties up capital.

These case studies validate the 2026 strategy: USDC is no longer an experimental alternative but a core infrastructure component for remittance corridors where speed and cost are the primary drivers of user choice.

Key risks and regulatory considerations

Sending money across borders using USDC isn't just about speed; it's about trust. The core promise of USDC is that every token is backed one-to-one by cash and short-dated U.S. Treasuries, held in segregated accounts for the benefit of holders [[src-serp-7]]. This structure is designed to keep the peg stable, but it relies entirely on the integrity of the custodians holding those reserves.

Regulatory oversight is the other side of that coin. While USDC is issued by Circle, a regulated financial institution, the broader landscape of stablecoin compliance is shifting rapidly. You need to ensure your remittance provider is fully compliant with local AML (Anti-Money Laundering) and KYC (Know Your Customer) laws. A provider like Stripe, for example, handles the crypto complexity behind the scenes, allowing businesses to send and receive USDC without directly touching the underlying blockchain [[src-serp-4]]. This reduces your operational risk but introduces counterparty risk—you're trusting their infrastructure.

Transparency is non-negotiable. Reputable issuers publish monthly attestation reports from independent accounting firms. If a provider can't show you these reports, or if they use vague "reserves" that include commercial paper or private equity, walk away. In high-stakes remittance, visibility into the reserve composition is your only real protection against de-pegging events.

Frequently asked questions about USDC remittances

What are the total costs of sending $100 via USDC compared to Western Union?

Sending $100 via Western Union typically incurs a transfer fee of $4–$8 plus a 3–5% foreign exchange spread, resulting in a total cost of $7–$13. In contrast, sending $100 via USDC on low-fee chains like Polygon or Solana costs less than $0.01 in network fees with zero FX spread. Even on Ethereum, where gas fees may range from $1–$10, the elimination of the FX spread often makes USDC cheaper for larger amounts or when comparing against high-spread traditional corridors.

How does USDC maintain its dollar peg?

USDC is issued by Circle, a regulated financial institution. Every USDC token is backed 1:1 by cash and short-duration U.S. Treasuries held in segregated accounts with U.S. regulated banks. Circle publishes monthly attestation reports from independent accounting firms (such as Deloitte) to verify that these reserves fully back the circulating supply, ensuring stability for remittance users.

Who can receive USDC remittances?

Recipients need a digital wallet that supports USDC on the specific blockchain network used (e.g., Polygon, Solana, or Ethereum). Unlike traditional services that allow cash pickup at physical locations, USDC requires the recipient to have internet access and a compatible wallet. However, many remittance providers now offer "on-ramp" services where the recipient can instantly convert received USDC into local fiat currency deposited into their bank account or mobile money wallet.

Is USDC remittance safe from fraud or reversals?

USDC transactions are irreversible. Once sent, they cannot be canceled or reversed, which protects merchants from chargeback fraud but means users must be vigilant about recipient addresses. Traditional services like Western Union offer some dispute resolution and fraud protection, but USDC users must rely on the security of their own wallet practices and the compliance standards of the remittance provider facilitating the on/off-ramp.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!