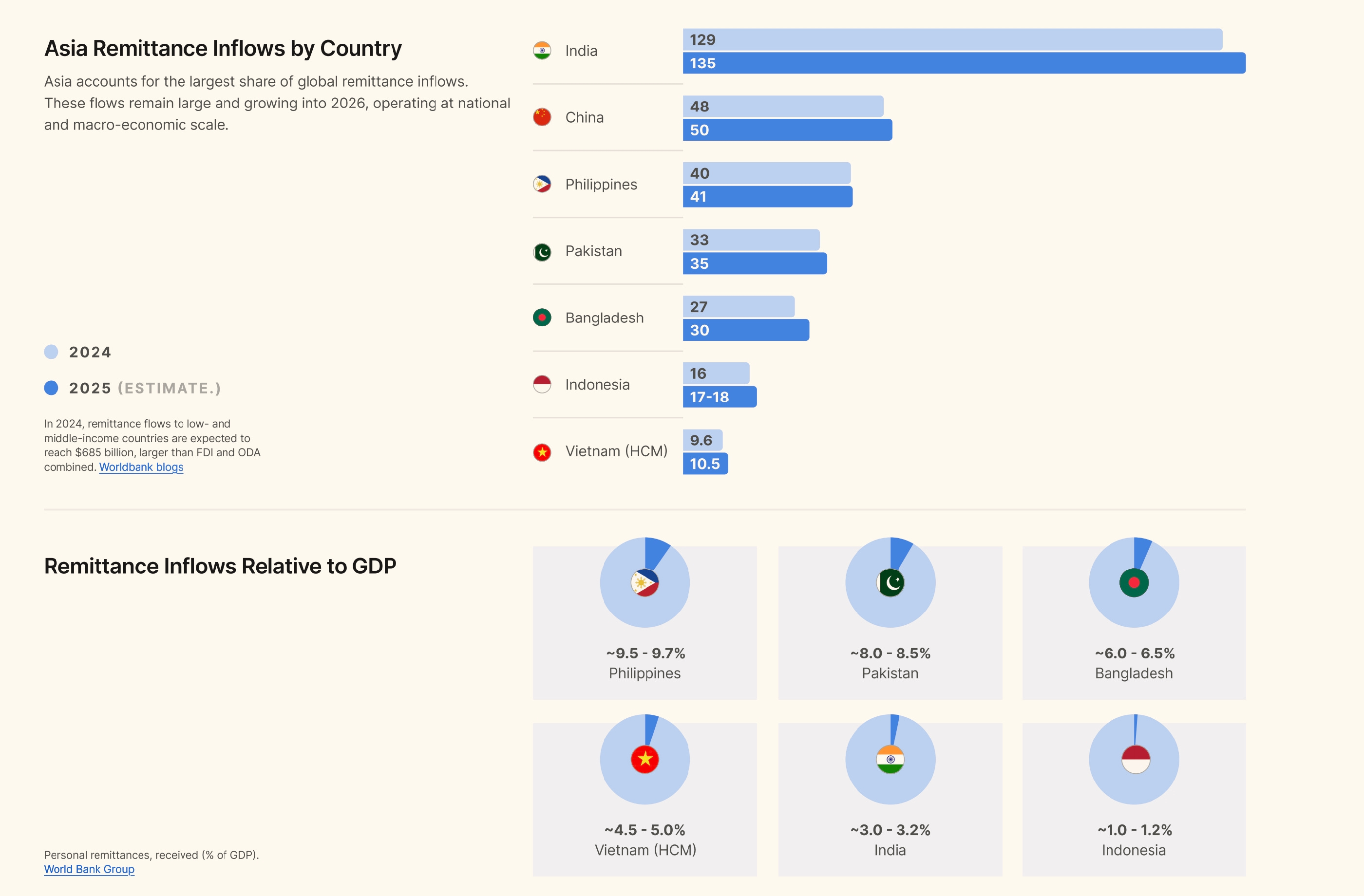

The USDC remittance strategy shift

The conversation around stablecoins is moving past speculation into operational reality. USDC is increasingly becoming the default infrastructure for cross-border settlements, driven by a combination of regulatory clarity and institutional adoption. This shift is not just about speed; it is about building a reliable, transparent ledger for global finance.

At its core, the USDC remittance strategy relies on a simple mechanism: converting local currency into a digital dollar, transmitting it across a blockchain network in minutes, and converting it back on the other side. This process removes the friction of traditional correspondent banking. Unlike volatile cryptocurrencies, USDC maintains its value through full backing by US dollar-denominated assets held in segregated accounts, ensuring stability for both senders and receivers.

Major financial platforms are integrating this infrastructure directly into their workflows. For instance, Stripe now allows businesses to send and receive USDC without needing to manage private keys or interact with complex crypto exchanges. This integration signals a broader trend where stablecoins are becoming a backend utility rather than a speculative asset.

To understand the current state of this market, it is helpful to look at the asset itself. While USDC is pegged to the US dollar, observing its performance against traditional markets provides context for its stability and liquidity.

This stability is what makes USDC particularly attractive for remittance corridors where speed and cost efficiency are critical. As more enterprises adopt these tools, the USDC remittance strategy is solidifying as a standard for modern cross-border payments.

Infrastructure upgrades driving speed

The bottleneck in global remittances has never been the lack of demand, but the sluggishness of the underlying settlement rails. Historically, cross-border payments relied on a fragmented chain of correspondent banks, where each intermediary required reconciliation and compliance checks. This structure meant that "same-day" transfers often landed days later, with fees eating into the principal along the way. The introduction of USDC as a settlement layer changes this dynamic by replacing the relay race with a direct flight path.

At the core of this acceleration is the Circle Payments Network (CPN). Rather than forcing remittance providers to build their own complex blockchain infrastructure from scratch, the CPN provides a unified, compliant gateway. It allows financial institutions to interact with USDC on multiple blockchains—such as Solana, Ethereum, and Polygon—through a single API. This abstraction layer is critical for enterprise adoption because it handles the heavy lifting of compliance, liquidity management, and cross-chain routing. For a remittance company, this means they can offer near-instant settlement without maintaining separate engineering teams for every supported blockchain.

Beyond the network layer, the deployment of non-custodial wallets has removed another significant friction point: the need for users to hold cryptocurrency. Early stablecoin adoption required recipients to manage private keys and navigate complex wallets, a barrier that excluded the unbanked and underbanked populations that remittances primarily serve. Innovations from partners like MoneyGram and Stellar have introduced non-custodial wallets that bridge this gap. These wallets allow users to receive USDC and instantly convert it to local fiat currency at a point of sale or bank deposit, without ever needing to understand how blockchain technology works.

This shift from "crypto-first" to "fiat-out" infrastructure is what makes USDC viable for mass-market remittances. The technology operates in the background, providing the speed and transparency of blockchain, while the user experience remains as simple as sending money through a familiar app. As these integrations mature, the cost and time disparities between traditional wire transfers and stablecoin rails will likely widen, making USDC not just an alternative, but the preferred infrastructure for global value transfer.

Cost analysis: USDC vs traditional rails

When sending money across borders, the traditional banking system is like a cargo ship: reliable, but slow and expensive. It moves through a series of intermediary banks, each taking a cut and adding days to the settlement time. USDC infrastructure, by contrast, operates more like a direct flight. By bypassing correspondent banking networks, it significantly reduces both the friction and the fees associated with cross-border payments.

The difference is most stark when looking at specific corridors, such as remittances to Colombia. Traditional money transfer operators often charge fees ranging from 5% to 10% for transactions under $500, plus hidden exchange rate markups that can add another 2-3% to the cost. A $100 transfer might end up costing the sender $12 or more in total fees and spread. This is particularly burdensome for migrant workers sending money home, where every percentage point matters.

USDC transfers flatten this cost curve. On-chain fees for stablecoins like USDC are typically fractions of a cent, regardless of the transaction size. While there are still costs to convert fiat to USDC and USDC back to local currency (fiat on/off ramps), the total cost is often less than 1% of the transaction value. For an SME or an individual sending $1,000, this can mean saving $50 to $100 per transaction compared to traditional rails.

Speed is another critical component of cost. Traditional wires can take 2-5 business days to settle, exposing senders and receivers to currency volatility during that window. USDC transfers settle in minutes. This near-instant settlement allows recipients to access working capital faster and reduces the risk of loss due to exchange rate fluctuations. For businesses, this liquidity advantage is often worth more than the direct fee savings alone.

The following table breaks down the typical differences between traditional remittance services and USDC-based infrastructure across key metrics:

| Metric | Traditional Rails | USDC Infrastructure |

|---|---|---|

| Average Fee | 5-10% | <1% |

| Settlement Time | 2-5 Business Days | <10 Minutes |

| Exchange Rate Markup | 2-3% | 0-0.5% |

| Accessibility | Requires Bank Account | Requires Smartphone & Wallet |

| Volatility Risk | High (during delay) | Low (instant settlement) |

Market research and adoption trends

The infrastructure upgrades powering USDC are already reshaping how money moves across borders. Market research indicates a clear shift from speculative crypto usage to practical, high-volume financial utility. This section summarizes the current adoption rates, focusing on SME integration, specific corridor performance, and the regulatory clarity that makes these transactions viable in 2026.

SME Usage and Corporate Treasury

Small and medium enterprises (SMEs) are increasingly adopting USDC for cross-border payments and payroll. Unlike traditional banking rails that can take days to settle, USDC allows for near-instant finality. This speed reduces the working capital tied up in transit, a critical advantage for businesses operating on thin margins. Corporate treasury departments are also leveraging USDC for onchain yield generation and merchant settlement, treating it as a stable, programmable dollar rather than a volatile asset.

Key Corridors and Remittance Flows

Remittance corridors, particularly in Latin America, are seeing significant traction. Initiatives like the partnership between MoneyGram and Stellar demonstrate how non-custodial wallets can bridge the gap between crypto and fiat currency. By using USDC to settle transactions, providers can speed up transfers while maintaining compliance. The typical flow involves the sender converting local currency to USDC, transmitting it across a blockchain network within minutes, and the recipient converting it back to local fiat. This model reduces friction and cost compared to legacy remittance services.

Regulatory Clarity and Market Stability

Regulatory clarity remains the backbone of this adoption. USDC’s commitment to being backed by the equivalent value of US dollar-denominated assets held in segregated accounts provides the trust necessary for institutional and retail use. This transparency is not merely theoretical; it represents actual assets held for the benefit of holders, ensuring that the stablecoin maintains its peg and liquidity even during market stress. As regulations evolve, this foundation of compliance positions USDC as a preferred instrument for cross-border commerce.

Key questions on stablecoin remittances

Understanding the mechanics of stablecoin remittances helps clarify why infrastructure upgrades matter for 2026. Below are direct answers to the most common questions about how these systems work and stay reliable.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!