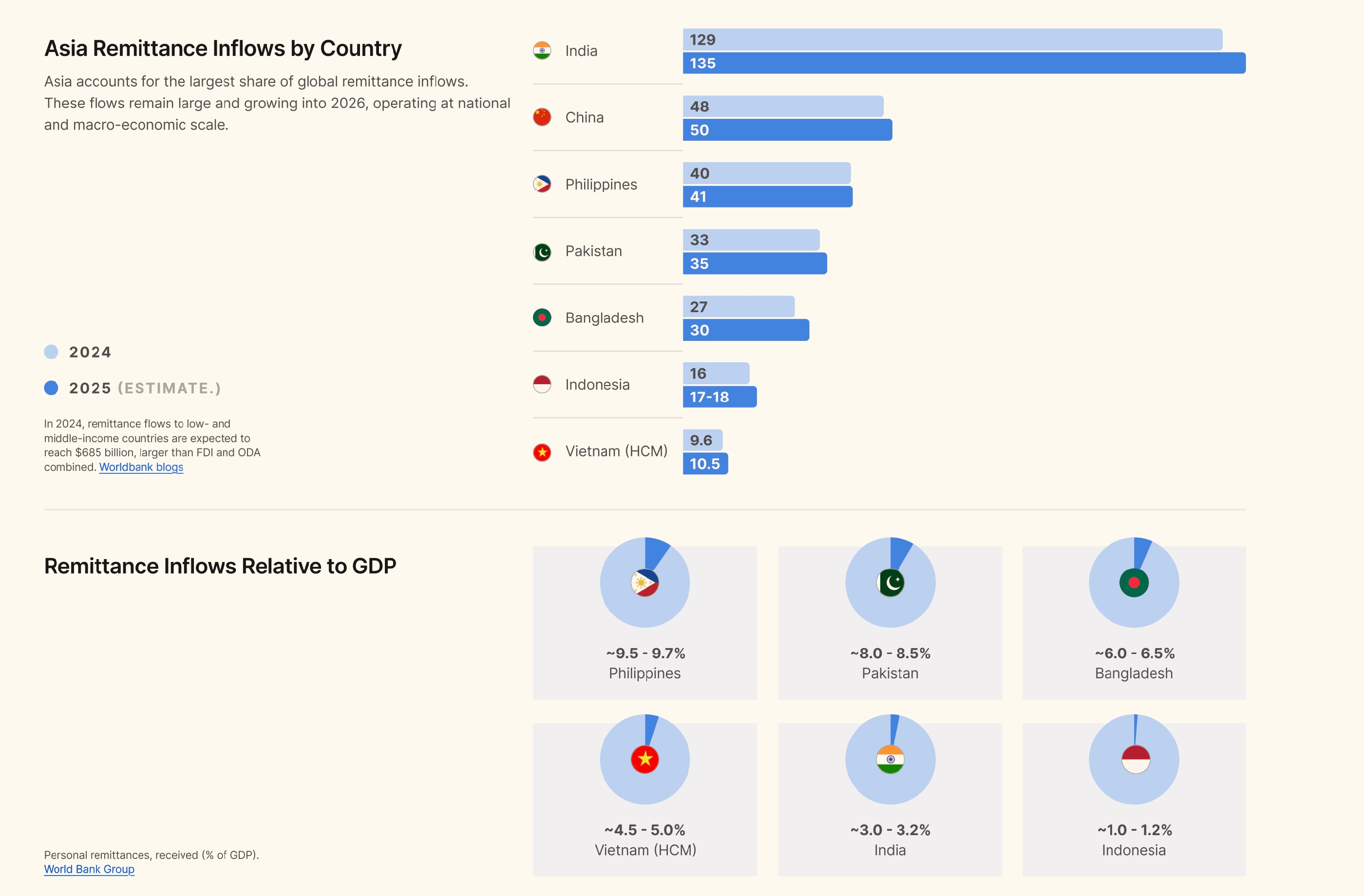

Why USDC remittance strategy matters now

The economics of moving money across borders have not changed much in decades, but the technology to fix them has. Traditional fiat rails charge an average of 5% to 7% in fees, a toll that eats into the livelihoods of millions of recipients. USDC infrastructure offers a stark alternative, reducing costs to under 1% while settling transactions in minutes rather than days. This gap is no longer theoretical; it is a operational reality that businesses and individuals are already exploiting.

The shift is driven by the mechanics of stablecoin remittances. In this flow, a sender converts local currency into a stablecoin and transmits it across a blockchain network. The recipient then converts it back into local currency. Unlike the multi-day clearance cycles of correspondent banking, this process happens on-chain, bypassing the intermediary banks that add both time and cost to every step. As highlighted by Circle, integrations with providers like BCRemit are already redefining the experience for users, making transfers faster and more accessible.

For a 2026 market analysis, the urgency lies in the compounding effect of these savings. In a high-stakes financial environment, preserving capital through efficient rails is not just a convenience; it is a strategic imperative. The ability to move value without the friction of legacy systems allows for better liquidity management and broader financial inclusion.

The market is responding to this efficiency. While traditional remittance corridors remain sticky due to regulatory inertia, the demand for cheaper, faster alternatives is growing. The data suggests that USDC is not just a speculative asset but a functional utility for cross-border payments. As regulatory frameworks evolve, the infrastructure built on USDC is positioned to capture a significant share of this market, offering a reliable, transparent, and cost-effective solution for global money movement.

USDC vs traditional money transfer costs

Traditional remittance corridors are expensive because they rely on a chain of correspondent banks and legacy infrastructure. Each intermediary takes a cut, and foreign exchange (FX) spreads often hide the true cost of the transfer. When you send money via Western Union or through the SWIFT network, you are paying for speed and physical presence, but the total cost can easily exceed 6% of the transfer amount, especially for smaller sums.

USDC changes this equation by removing the middlemen. By moving value on a blockchain, you bypass the correspondent banking network entirely. The cost becomes predictable: a small network gas fee plus the exchange rate difference. According to Stripe’s analysis of stablecoin cross-border payments, this infrastructure shift significantly reduces risk and frees up capital that was previously tied up in transit delays.

The table below breaks down the operational realities of both methods. While traditional services offer ubiquity, USDC offers transparency and speed that incumbents struggle to match.

| Metric | Traditional (Western Union/SWIFT) | USDC Rail |

|---|---|---|

| Cost | 3–10% (avg 6.3% globally) | |

| Cost | 0.5–2% (network + exchange fees) | |

| Speed | 1–5 business days | |

| Speed | Minutes | |

| FX Spread | High (hidden margin) | |

| FX Spread | Low (market rate) | |

| Tracking | Limited, branch-dependent | |

| Tracking | Real-time blockchain explorer |

The data shows a clear divergence in efficiency. For remitters moving funds to countries like Colombia, where peso volatility is a concern, USDC allows for near-instant conversion and settlement. This speed reduces exposure to currency swings that can erode the value of a transfer while it is in transit. Traditional methods simply cannot offer this level of immediacy without charging a premium that is rarely justified by the service quality.

How stablecoin remittance infrastructure works

Stablecoin remittances replace the multi-day banking corridor with a three-step digital workflow. The process moves from fiat on-ramp to blockchain transfer, and finally to fiat off-ramp. This architecture cuts out correspondent banks, reducing both time and cost. The technical flow relies on regulated intermediaries to bridge the gap between traditional finance and public blockchains.

The sender initiates the transfer by depositing local currency into a regulated exchange or payment processor. Before any tokens are issued, the platform performs Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. Once verified, the platform converts the fiat into USDC, minting or releasing the equivalent digital assets onto the blockchain. This step ensures that the origin of funds is traceable and compliant with local regulations.

USDC moves across a blockchain network, typically Ethereum, Solana, or Polygon. Unlike traditional wire transfers, this step does not involve intermediary banks. The transaction is recorded on the public ledger, providing real-time tracking. Circle, the issuer of USDC, maintains a 1:1 reserve of cash and short-term US Treasuries, ensuring the token’s stability. The transfer usually settles in seconds to minutes, regardless of the destination country or time of day.

The recipient’s platform receives the USDC and converts it back into local currency. This off-ramp process mirrors the on-ramp, requiring identity verification before the fiat is disbursed. The recipient can withdraw funds to a local bank account, a mobile wallet, or a cash pickup location. Intermediaries like Stripe or local fintech partners facilitate this final step, ensuring the payout complies with regional banking laws.

The reliability of this infrastructure depends on the stability of the underlying asset. USDC’s price peg to the US dollar minimizes exchange rate risk during the transfer window. This stability is critical for remittance recipients who rely on predictable purchasing power.

Regulatory compliance is the backbone of this system. Intermediaries must adhere to strict reporting standards, including the Travel Rule for cross-border payments. This ensures that every transaction is linked to a verified sender and recipient, reducing the risk of illicit finance while maintaining the speed and efficiency benefits of blockchain technology.

Real-world case studies in cross-border payments

Theoretical benefits of USDC remittances become tangible when applied to live financial infrastructure. Three providers—BCRemit, Onafriq, and MuralPay—demonstrate how stablecoins replace traditional correspondent banking rails for specific use cases. Each company leverages Circle’s USDC to solve distinct friction points: speed for African corridors, cost for Latin American remittances, and liquidity for SMEs.

BCRemit: Redefining accessibility

BCRemit has integrated Circle’s USDC to overhaul the remittance experience for its users. By moving value on-chain, the company delivers transfers that are faster, cheaper, and more accessible than legacy methods. This approach removes the delays inherent in multi-bank intermediaries, allowing senders to reach recipients with near-instant settlement. The result is a streamlined flow that prioritizes user experience over traditional banking bureaucracy.

Onafriq: Simplifying African corridors

Onafriq partners with Circle to enhance cross-border remittances into Africa. The collaboration simplifies global payments by leveraging USDC to bypass the fragmentation of local banking networks. For senders targeting African recipients, this partnership reduces the complexity and cost associated with traditional wire transfers. The model highlights how stablecoins can serve as a universal bridge currency in regions where local fiat infrastructure is underdeveloped or expensive to access.

MuralPay: Protecting SME working capital

MuralPay focuses on the specific needs of small and medium-sized enterprises (SMEs) sending money to Colombia. By pairing virtual USD accounts with near-instant USDC on-chain transfers, the platform provides faster access to working capital. Crucially, this method reduces exposure to peso volatility. Unlike traditional money transfers that may take days to settle, MuralPay’s USDC integration allows businesses to manage liquidity in real-time, protecting margins from currency fluctuations during the transfer window.

Regulatory compliance and risk management

Stablecoin remittances operate in a high-stakes regulatory environment. Because USDC is a fully reserved, dollar-pegged asset, its utility for cross-border payments depends heavily on the issuer's adherence to strict legal standards. Circle maintains full reserve holdings and undergoes regular attestation, which provides the transparency required for institutional and high-volume remittance flows. This compliance framework is essential for mitigating counterparty risk and ensuring that funds remain accessible and stable during transit.

At the transaction level, anti-money laundering (AML) and know-your-customer (KYC) protocols are non-negotiable. A typical stablecoin remittance flow involves the sender converting local currency to a stablecoin, transmitting it across a blockchain network, and the recipient converting it back. While the blockchain layer offers speed, the on-ramp and off-ramp services must verify identities to comply with federal and international regulations. Failure to integrate robust compliance checks can lead to frozen assets or legal penalties, turning a fast payment into a logistical nightmare.

Using regulated issuers like Circle reduces operational friction for businesses and individuals alike. Unlike unregulated tokens, USDC’s compliance posture allows it to integrate seamlessly with traditional financial infrastructure, including banking partners and payment processors. This regulatory alignment ensures that USDC remittance strategies remain viable even as global financial authorities tighten oversight on digital asset flows.

Frequently asked questions about USDC remittances

How does stablecoin remittance work?

In a typical stablecoin remittance flow, the sender converts local currency to a stablecoin and transmits it across a blockchain network within minutes. The recipient then converts it back into local currency. This process bypasses traditional correspondent banking rails, significantly reducing settlement times from days to seconds.

Is USDC regulated for cross-border transfers?

USDC is issued by Circle, a regulated financial institution headquartered in the United States. Unlike decentralized stablecoins, USDC reserves are held in cash and short-term U.S. Treasury securities, with regular attestation reports published monthly. This regulatory framework provides a layer of compliance and transparency that many institutional remittance providers require.

What are the fees compared to traditional services?

Traditional remittance services often charge a percentage of the transfer amount plus fixed fees, which can exceed 6% for smaller transfers. USDC transactions typically involve minimal network gas fees and lower provider spreads. For high-volume business remittances, this cost difference can translate into substantial savings over time.

Can I send USDC to anyone?

Recipients must have a digital wallet that supports USDC on the specific blockchain network you are using (such as Ethereum, Solana, or Polygon). While the technology is open, the recipient needs to be comfortable with crypto onboarding. Many remittance apps now simplify this by handling the wallet creation and fiat conversion on the backend.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!