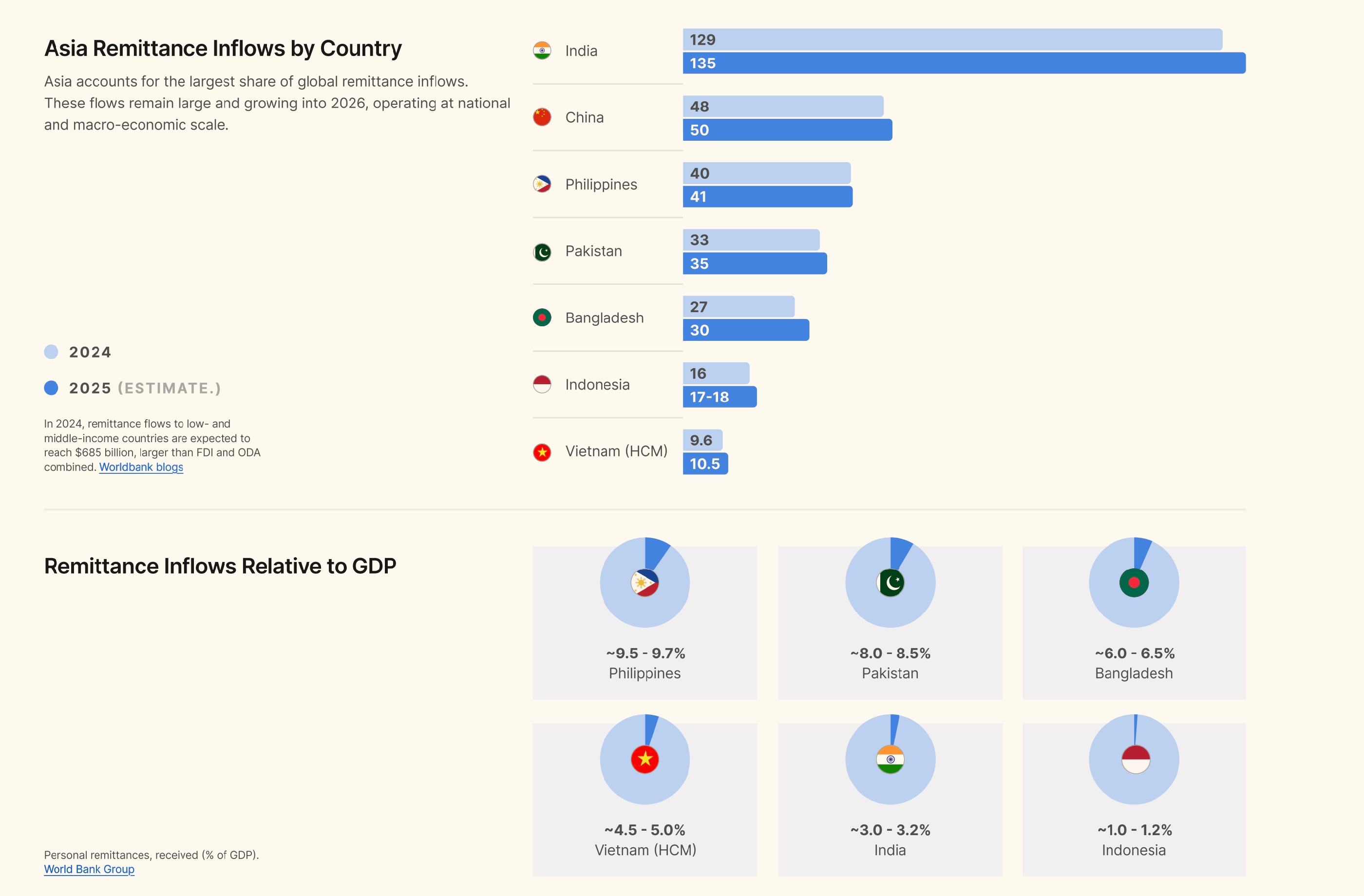

Why USDC changes remittance math

Traditional cross-border payments operate on legacy rails like SWIFT, which were built for banks, not individuals. This infrastructure often requires days to settle and involves multiple intermediary banks, each taking a cut. The result is high fees and unpredictable exchange rates that erode the value of the money being sent.

USDC shifts this model by leveraging blockchain technology to move value directly between sender and recipient. Because USDC is a stablecoin pegged 1:1 to the US dollar, it eliminates the volatility risk associated with other cryptocurrencies. Every unit of USDC is backed by cash and short-dated U.S. Treasuries held in regulated financial institutions, with monthly attestations from independent auditors to ensure transparency [Circle].

The economic impact for the user is immediate. Industry analyses suggest that senders can cut fees by up to 50% compared to traditional money transfer services like Western Union [Muralpay]. Instead of waiting three to five business days, transactions typically settle in minutes. This speed and cost efficiency make USDC a compelling alternative for families relying on remittances to support their households.

To understand the current market context, it helps to see how USDC trades against the dollar.

How USDC remittance infrastructure works

USDC remittance relies on a three-part chain: fiat on-ramp, blockchain transfer, and fiat off-ramp. This flow replaces traditional correspondent banking with digital rails that move value in minutes rather than days. The infrastructure is built on stablecoin protocols, primarily Circle's USDC, which maintains a 1:1 peg with the U.S. dollar.

The sender converts local currency into USDC. This happens through a regulated fintech or payment provider that holds the fiat in reserve and mints the corresponding stablecoin. Services like Stripe enable businesses to execute this without managing private keys directly, bridging traditional banking with digital assets [src-serp-5].

The USDC moves across a blockchain network, such as Solana, Ethereum, or Stellar. This step is where the speed advantage emerges. Transactions settle in seconds or minutes with fees often below a cent, regardless of the distance between sender and recipient. The value remains stable because USDC is backed by cash and short-dated U.S. Treasuries [src-serp-6].

The recipient converts USDC back into their local currency. This happens through a partner network that accepts stablecoins and deposits fiat directly into a bank account or mobile wallet. The recipient never needs to interact with crypto wallets or exchanges, ensuring the experience feels like a standard money transfer [src-serp-6].

This closed-loop model is the standard for most remittance companies adopting stablecoins. It minimizes regulatory friction by keeping fiat custody within regulated entities while leveraging blockchain for settlement. The result is a system that combines the speed of digital assets with the familiarity of traditional banking.

USDC vs traditional money transfer costs

When sending money across borders, the headline fee is rarely the whole story. Traditional providers like Western Union, MoneyGram, and banks often advertise low transfer fees but make up the difference with hidden markups on the exchange rate. These spreads can easily add 3-5% to the total cost, meaning you send $100 but the recipient gets significantly less than expected.

USDC transfers operate differently. By moving value on a blockchain network, you bypass the correspondent banking system that adds layers of fees and delays. The cost is primarily determined by the network transaction fee (gas) and the platform's flat fee, which is usually a fixed small amount rather than a percentage of the transfer. This structure becomes increasingly advantageous as transfer sizes grow, as the percentage cost drops sharply compared to legacy services.

According to industry analyses, senders can cut fees by up to 50% compared with traditional money transfer providers when using stablecoins for routes like remittances to Colombia. While traditional providers are integrating crypto solutions—such as MoneyGram and Stellar's non-custodial wallets—the direct USDC transfer remains the most cost-effective baseline for independent users.

The table below breaks down the typical cost structures for a $500 transfer to a major Latin American market, based on current industry averages.

| Provider Type | Typical Fee | Exchange Rate Markup | Settlement Time |

|---|---|---|---|

| USDC (Direct) | $1-$5 (Network + Platform) | ~0% (if pegged) | Minutes |

| Traditional Bank | $15-$30 | 3-5% | 1-3 Days |

| MoneyGram / Western Union | $5-$15 | 2-4% | Minutes - Hours |

| Wise / Remitly | $3-$8 | 0.5-1% | Hours - Days |

Real-world USDC remittance case studies

Theoretical benefits of stablecoins only prove their worth when they survive contact with real-world friction. Two recent partnerships demonstrate how USDC is moving from pilot programs into active cross-border payment rails.

BCRemit has integrated Circle’s USDC to streamline its remittance infrastructure. By replacing traditional correspondent banking networks with a blockchain-based settlement layer, BCRemit reduces the time and cost associated with moving funds across borders. The result is a faster, cheaper experience for users who previously faced delays and high fees. Circle’s case study on BCRemit details the technical integration and the operational improvements achieved.

Similarly, Onafriq has partnered with Circle to power remittances into Africa. This collaboration aims to simplify global payments by leveraging USDC’s stability and speed. For corridors where traditional banking infrastructure is sparse or expensive, stablecoins offer a direct alternative that bypasses multiple intermediaries. Onafriq’s announcement with Circle highlights the focus on enhancing accessibility for underserved markets.

These examples show that USDC is not just a speculative asset but a functional tool for settlement. The key advantage lies in the ability to move value instantly while maintaining a 1:1 peg to the US dollar, providing the predictability required for both senders and receivers.

Regulatory risks and reserve backing

When you build a USDC remittance strategy for 2026, the safety of your capital depends on two things: the regulatory environment and the quality of the reserves holding your funds. Unlike volatile cryptocurrencies, USDC is a fiat-backed stablecoin designed to maintain a steady $1.00 value, but this stability requires strict oversight.

Circle, the issuer of USDC, publishes monthly attestations from a Big Four accounting firm to verify these reserves. This transparency is critical for remittance, where trust is the primary product. If the reserves were not liquid and fully backed, the entire mechanism would collapse under the weight of redemption requests.

Regulatory risks remain the biggest variable. The U.S. government is actively debating stablecoin legislation, which could change how issuers operate or how you report transactions. However, because USDC holds its assets in regulated U.S. banks rather than offshore havens, it currently faces a clearer legal path than many competitors. For a remittance strategy, this means your funds are exposed to U.S. financial regulations, which offers protection but also requires you to stay compliant with evolving AML (Anti-Money Laundering) standards.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!