Why USDC dominates cross-border rails

The traditional remittance market has long been defined by friction. Sending money across borders often involves multiple intermediaries, opaque fees, and settlement times that stretch over days. USDC has emerged as a dominant force in this space by offering a digital alternative that aligns with modern infrastructure needs. It provides a stable, dollar-pegged asset that moves at the speed of the internet rather than the speed of the banking system.

Speed and Cost Efficiency

The most immediate advantage of using USDC for remittances is the dramatic reduction in time and cost. According to Circle, the issuer of USDC, the World Bank has found that the average cost of sending cross-border remittances exceeds 6%, with nearly half of all transfers costing more than that threshold. Traditional fiat rails often add layers of correspondent banking fees and foreign exchange spreads on top of these base costs.

USDC transactions typically settle in seconds or minutes, regardless of the time of day or day of the week. This immediacy is critical for individuals who rely on remittances for daily living expenses. By bypassing the slow legacy clearing systems, USDC allows funds to move directly from sender to receiver, significantly lowering the total cost of the transaction. This efficiency is not just a technical improvement; it is a substantial economic benefit for the billions of people who send money home each year.

Regulatory Clarity and Trust

Beyond speed and cost, USDC’s dominance is built on a foundation of regulatory clarity. Unlike many cryptocurrencies that operate in gray areas, USDC is issued by Circle, a regulated financial institution. This regulatory adherence provides a level of trust and stability that is essential for institutional adoption and mainstream usage. Users and businesses can rely on the fact that USDC is fully backed by cash and short-dated U.S. treasuries, ensuring that the peg remains stable.

This regulatory framework reduces the counterparty risk associated with other digital assets. For remittance providers and financial institutions, integrating USDC means working within a known legal and compliance structure. This clarity facilitates partnerships with traditional banks and payment processors, further expanding the reach and utility of USDC in the global remittance market.

Mapping the settlement infrastructure

USDC remittances rely on a specific stack of on-chain networks and fiat rails to function. The infrastructure isn't a single monolithic chain; it is a distributed network where different blockchains serve different geographic and economic needs. For cross-border payments, speed and cost are determined by which network handles the transfer and which partner manages the fiat exit.

Base and Stellar: The Primary Chains

Two networks dominate the current USDC remittance landscape: Base and Stellar. Each serves a distinct purpose in the settlement flow.

Base has seen explosive growth in high-value transfers. Daily USDC transfers exceeding $100,000 on Base grew from under 50,000 to over 450,000 in January 2026, dwarfing activity on other networks [Talos]. This surge suggests that Base is becoming the preferred rail for institutional or high-volume remittance corridors where finality speed and low fees matter most.

Stellar, in partnership with the Stellar Development Foundation, focuses on accessibility. It enables more than a billion dollars in USDC remittance volume for millions of customers worldwide [Arf.one]. Stellar’s infrastructure is often integrated with local payment providers, making it easier to convert USDC directly into local currency for end-users in emerging markets.

Fiat On/Off-Ramps

The blockchain is only half the equation. The value of USDC in remittances is realized when it converts to local fiat. This conversion happens through licensed on-ramps and off-ramps like BCRemit. By integrating Circle's USDC, partners like BCRemit have redefined the remittance experience, making it faster and cheaper than traditional banking rails [Circle]. These partners handle the regulatory compliance and local liquidity, bridging the gap between the digital asset and the recipient's bank account or mobile wallet.

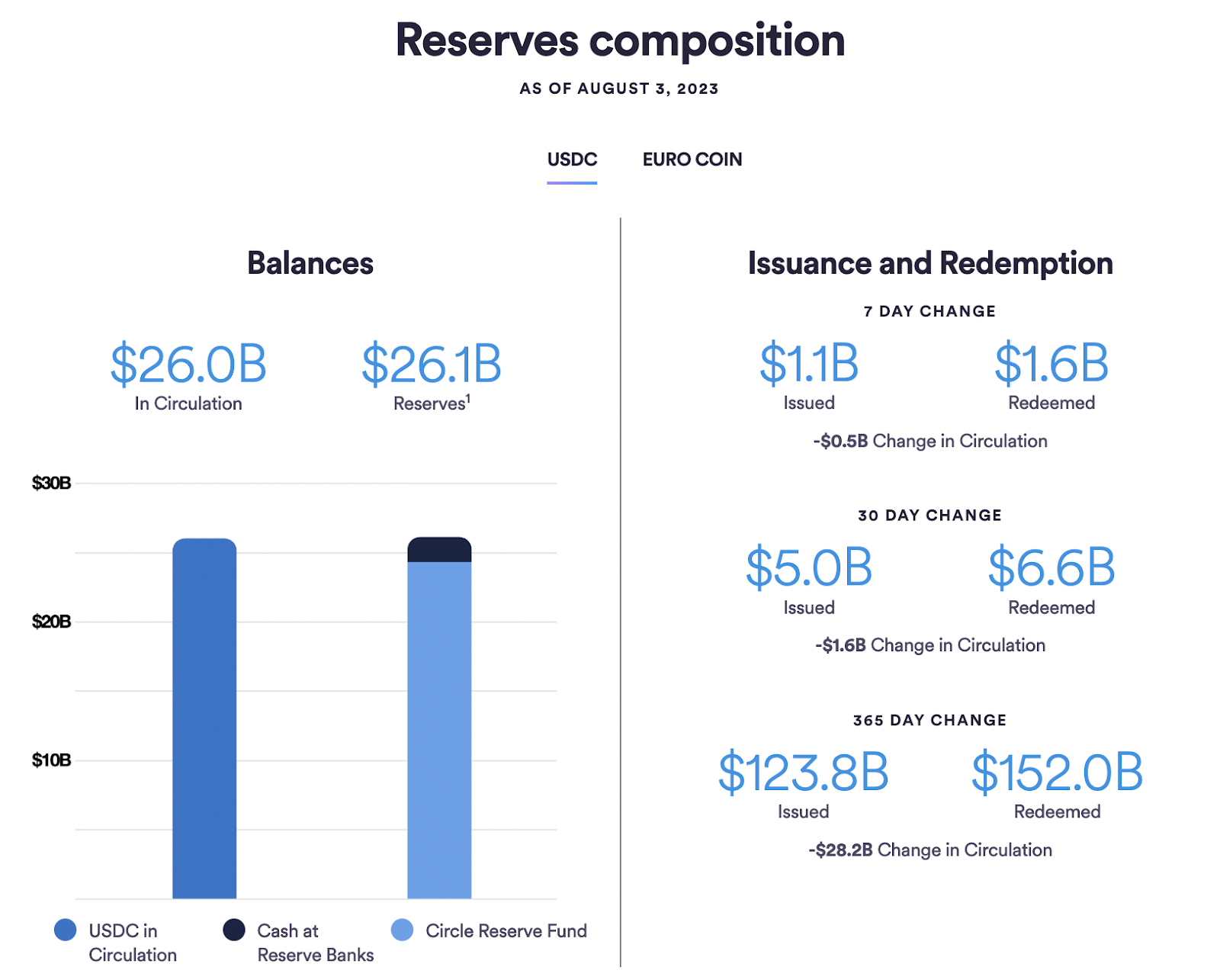

Market Context

The scale of USDC in remittances is significant. The following chart shows the market performance and volume trends that underpin this infrastructure.

Cost and speed metrics in 2026

The gap between traditional remittance corridors and stablecoin infrastructure has widened significantly. In 2026, USDC offers a structural advantage in both settlement velocity and fee transparency, addressing the inefficiencies that have long plagued cross-border payments. While traditional banking networks rely on correspondent banking chains that introduce delays and hidden FX markups, USDC operates on a direct ledger model.

The World Bank’s latest data indicates that the average cost of sending cross-border remittances remains stubbornly high, often exceeding 6% globally. In contrast, on-chain USDC transfers typically incur network gas fees that are fractions of a cent, regardless of the transfer amount. This disparity is most pronounced for smaller, high-frequency transactions common in payroll and gig economy payouts.

Settlement time follows a similar divergence. Traditional wire transfers often require one to three business days to clear, depending on the origin and destination countries. USDC settlements occur in seconds, independent of banking hours or holidays. This immediacy reduces counterparty risk and improves cash flow for recipients who rely on timely access to funds.

The following comparison illustrates the operational differences between a standard international wire and a USDC transfer across key metrics.

| Metric | Traditional Wire | USDC Transfer |

|---|---|---|

| Average Fee | >6% (World Bank avg) | <$0.01 (network dependent) |

| Settlement Time | 1-3 business days | <10 seconds |

| Accessibility | Requires bank account | Requires digital wallet |

| Transparency | Hidden FX markups | On-chain visibility |

While traditional methods offer regulatory familiarity, the cost and speed advantages of USDC are now measurable facts rather than theoretical promises. For businesses and individuals prioritizing efficiency, the infrastructure is ready to support these shifts at scale.

Strategic use cases for businesses

Enterprises are moving beyond experimental pilots to deploy USDC for three core operational needs: payroll, treasury management, and market entry in high-inflation regions. The strategy is no longer about speculation; it is about replacing broken legacy rails with programmable, settlement-final infrastructure.

Cross-Border Payroll

Traditional cross-border payroll involves multiple intermediaries, each taking a cut and delaying settlement by days. USDC collapses this chain. By paying contractors and employees directly in stablecoins, companies reduce settlement times from T+2 to minutes, regardless of the recipient’s location. This is particularly valuable for global teams in regions with limited banking access or volatile local currencies. The friction of reconciliation drops significantly when the ledger is shared and transparent.

Treasury Management

For multinational firms, holding cash in traditional bank accounts often means losing value to inflation or negative interest rates. USDC offers a way to park idle treasury funds in a dollar-pegged asset that generates yield through money market funds or lending protocols, without exposing the balance sheet to the volatility of Bitcoin or Ethereum. This turns idle cash into a productive asset while maintaining liquidity for immediate operational needs.

High-Inflation Market Entry

In economies with hyperinflation, local currency instability can erase profit margins overnight. USDC provides a stable unit of account for pricing goods and services. Companies operating in these markets can invoice in USDC, protecting their revenue from sudden devaluation. For consumers, receiving payments in USDC offers a hedge against local currency collapse, making it a powerful tool for building trust and adoption in emerging markets.

Essential tools for USDC remittance

Executing USDC remittances requires selecting the right infrastructure for your specific volume and security needs. The market has matured from experimental pilots to robust, enterprise-grade rails that handle billions in volume.

Top Platforms and Infrastructure

For high-volume business-to-business (B2B) transfers, platforms like BCRemit leverage Circle’s USDC infrastructure to offer faster, cheaper settlements compared to traditional banking rails. Their integration with Stellar allows for near-instant finality, making them a strong choice for payroll and supplier payments.

For individual senders, Stellar and Solana-based wallets provide low-cost entry points. These networks offer transaction fees of fractions of a cent, ensuring that small remittances remain economically viable. Always verify the receiving end’s support for USDC to avoid conversion friction.

Security Essentials

Self-custody is the gold standard for security. A hardware wallet like the Ledger Nano X or Trezor Safe 3 keeps your private keys offline, protecting your funds from exchange hacks or phishing attacks. For frequent travelers, a mobile hardware solution like the Ledger Stax offers convenient tap-to-sign functionality without compromising security.

As an Amazon Associate, we may earn from qualifying purchases.

Common questions about USDC remittances

Is USDC safe for sending money?

USDC is a regulated stablecoin pegged 1:1 to the US dollar, with reserves held in cash and short-term US Treasuries. This structure minimizes the volatility risk associated with cryptocurrencies like Bitcoin, making it a reliable store of value for cross-border transfers. However, users must still assess the compliance and security track record of the specific remittance provider or wallet they choose to use.

How fast are USDC transfers?

Unlike traditional bank wires that can take 3-5 business days to settle, USDC transactions typically confirm in minutes. Because these transfers occur on blockchain networks rather than through the SWIFT banking system, they bypass intermediate correspondent banks. This speed is particularly valuable for urgent payments and payroll disbursements in high-inflation economies where time-sensitive liquidity is critical.

Are USDC remittance fees lower than banks?

Yes. Traditional remittance services often charge high fixed fees plus unfavorable exchange rates. USDC transfers generally incur only network gas fees and minimal platform charges, which are often fractions of a cent on efficient networks like Stellar or Base. This cost efficiency allows senders to retain more of their principal, especially for smaller transaction amounts.

Is USDC legal for remittances in my country?

Regulatory status varies by jurisdiction. While USDC is legal in many regions, some countries restrict or ban cryptocurrency usage for cross-border payments. Users should verify local regulations regarding stablecoin adoption before initiating transfers. Providers like Circle and partners on the Stellar network operate within specific regulatory frameworks to ensure compliance where permitted.

No comments yet. Be the first to share your thoughts!