Why USDC leads cross-border payments

USDC has emerged as the dominant stablecoin for remittances because it bridges the gap between traditional finance infrastructure and blockchain efficiency. Unlike experimental crypto assets, USDC operates with a regulatory framework that institutions trust, ensuring that funds move quickly without the volatility that plagues other digital currencies.

The network effect is undeniable. Major payment processors like Stripe and Mastercard have integrated USDC, allowing remittance providers to tap into existing liquidity pools. This institutional adoption means lower friction for users. For example, services like BCRemit leverage Circle’s infrastructure to offer transfers that are significantly faster and cheaper than legacy wire systems, proving that the technology works at scale.

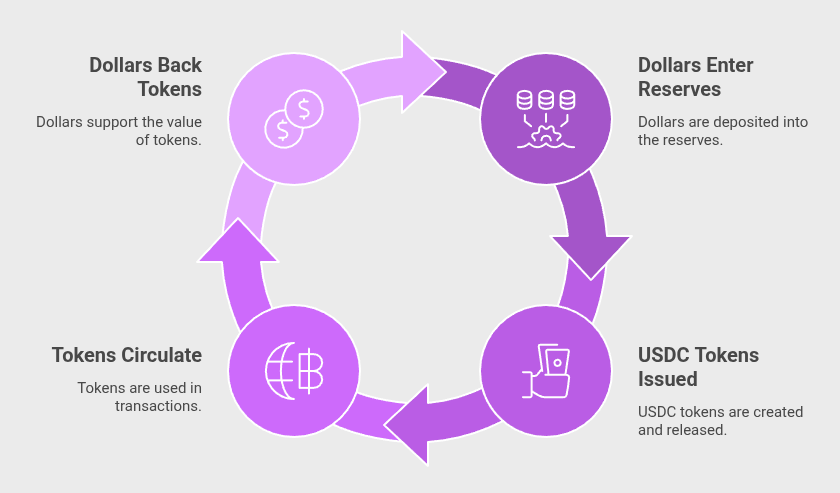

Stability is the core value proposition. A $1 USDC is consistently backed by cash and short-dated US Treasuries, maintaining a near-perfect peg to the dollar. This predictability is essential for remittances, where recipients rely on the exact value of the transfer to cover living expenses. While other stablecoins face scrutiny over their reserve composition, USDC’s transparency and regular attestation reports provide the certainty required for high-stakes financial decisions.

USDC vs. Traditional Money Transfer

When you send money across borders, you are essentially paying for two things: the time it takes for the funds to move and the risk that something goes wrong. Traditional providers like Western Union or MoneyGram have built their businesses on decades of physical infrastructure, while USDC remittances rely on blockchain rails. The difference isn't just technological; it is structural.

Traditional remittance networks operate on a correspondent banking model. This means your money often hops through multiple intermediary banks before reaching the recipient, each taking a cut and adding processing time. USDC, by contrast, moves directly from sender to recipient on the blockchain. This direct settlement reduces friction significantly. According to analysis of blockchain-powered platforms, USDC remittance models can cut transfer costs by up to 50% compared to legacy providers while delivering funds almost instantly rather than over several days.

The trade-off lies in accessibility. Traditional providers offer cash pickup options that do not require a smartphone or internet access, which remains critical in many emerging markets. However, the gap is closing. Major financial institutions are bridging this divide. Mastercard and MoneyGram, for example, have unveiled non-custodial wallets to bridge the worlds of crypto and fiat currency with USDC, allowing recipients to access digital assets without needing complex technical knowledge.

To understand the real-world impact, we can look at the core metrics that matter to senders: cost, speed, and availability.

| Metric | USDC | Traditional (e.g., WU/MG) |

|---|---|---|

| Typical Cost | < 1% (network fees only) | 5% - 10% + hidden FX margins |

| Settlement Time | Seconds to minutes | 1 - 3 business days |

| Availability | 24/7/365 | Limited hours / business days |

| Cash Pickup | Via partner networks | Extensive physical agent network |

The data shows a clear divergence. USDC offers near-instant settlement at a fraction of the cost, but it requires the recipient to have a digital wallet. Traditional providers offer a wider physical footprint for cash access but charge a premium for that convenience and the slower settlement times inherent in the legacy banking system.

Infrastructure upgrades driving efficiency

The speed of a remittance transfer is only as good as the rails it travels on. For USDC, those rails have expanded far beyond the original Ethereum mainnet. Today, USDC is live on more than a dozen blockchains, including Solana, Stellar, and Avalanche. This multi-chain strategy is not just about offering choices; it is a direct response to the need for lower costs and faster finality. By moving transactions to networks with higher throughput, remittance providers can bypass the congestion and high gas fees that often plague traditional Ethereum transfers.

This flexibility allows financial institutions to match the blockchain to the specific corridor. A transfer from the United States to the Philippines might leverage Stellar for its low fees, while a high-value corporate payment might utilize Ethereum Layer 2 solutions for added security and compliance tooling. The result is a scalable infrastructure that can handle volume spikes without breaking the bank. According to Circle, USDC is now available on over 30 blockchains, ensuring that no matter where the money needs to go, there is a path that is both fast and cost-effective.

The backend security of these systems has also evolved. Modern remittance platforms are increasingly adopting non-custodial wallet solutions and institutional-grade custody providers like Fireblocks. These tools allow users to retain control of their private keys while benefiting from enterprise-level security protocols. This shift reduces counterparty risk and ensures that funds are not sitting idle in centralized exchange accounts. Instead, the money moves directly from sender to recipient, minimizing the number of intermediaries that can slow down the process or charge hidden fees.

USDC operates across 30+ blockchains, allowing providers to select the network with the lowest fees and fastest settlement times for each specific corridor.

Partnerships with providers like Fireblocks enable secure, non-custodial wallet management, reducing counterparty risk while maintaining regulatory compliance.

Funds move directly between wallets on the blockchain, bypassing traditional correspondent banking networks and reducing the number of intermediaries.

The combination of multi-chain support and robust custody solutions has transformed USDC from a simple digital dollar into a sophisticated remittance infrastructure. For businesses, this means they can offer their customers a service that is not only faster than traditional wire transfers but also more transparent and cheaper to operate. As the technology matures, the gap between crypto-native efficiency and traditional banking security continues to narrow, making USDC a viable primary option for cross-border payments.

Compliance and regulatory considerations

In the high-stakes world of cross-border payments, regulatory compliance is not just a hurdle—it is the foundation of trust. For remittance companies, the margin for error is slim, and the cost of non-compliance can be existential. This is where USDC’s regulated status provides a distinct infrastructure advantage over unregulated alternatives.

Unlike decentralized cryptocurrencies that operate in regulatory gray areas, USDC is issued by Circle, a regulated financial institution. This means every token is backed by cash and short-dated US Treasury bills, and Circle is subject to rigorous audits and regulatory oversight. For remittance providers, this translates to a clearer path to meeting Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements. You are not building compliance on top of an opaque protocol; you are integrating with a financial asset that was designed with compliance in mind.

The practical impact is significant. When you integrate USDC, you are leveraging an infrastructure that already anticipates regulatory scrutiny. Circle’s commitment to transparency—through regular attestation reports and adherence to US federal money transmission laws—means your remittance platform can focus on speed and cost-efficiency rather than constantly mitigating regulatory risk. This is not just about avoiding fines; it is about building a sustainable, scalable business that banks and regulators view as a partner, not a liability.

While the broader crypto landscape remains fragmented, USDC’s position as a compliant, fiat-pegged asset offers a stable bridge between traditional finance and the efficiency of blockchain technology. For remittance companies, this means faster settlement times and lower costs without sacrificing the regulatory certainty required to operate in major markets.

Real-world case studies in adoption

Theory is easy; execution is where the infrastructure shows its teeth. Companies like BCRemit and MuralPay have moved past pilot programs to prove that USDC remittance strategy works in live markets. They aren't just talking about speed—they are shipping it.

BCRemit integrated Circle’s USDC to overhaul its global payout rails. The result was a direct reduction in settlement times and fees, making the service cheaper and more accessible for end users. By bypassing traditional correspondent banking layers, they demonstrated how stablecoin infrastructure can handle real volume without the latency of legacy systems.

In Latin America, the shift is equally tangible. MuralPay’s analysis of remittances to Colombia highlights a stark contrast between traditional money transfer costs and blockchain-powered alternatives. Industry data suggests that USDC models in this corridor can cut transfer costs by up to 50% while delivering funds almost instantly. This isn't a marginal improvement; it's a structural advantage for senders and receivers alike.

These examples underscore a broader market shift. As Mastercard and other financial giants explore non-custodial wallets and stablecoin bridges, the gap between traditional remittance and crypto-native settlement is closing. The technology is no longer experimental—it is the new standard for efficient cross-border value transfer.

Frequently asked questions about USDC remittances

What is stablecoin remittance?

Stablecoin remittance is a cross-border payment method where the sender converts local currency into a stablecoin like USDC and transmits it over a blockchain network. This process typically settles within minutes, bypassing traditional banking rails. The recipient then converts the stablecoin back into their local currency, significantly reducing the friction and time associated with international settlement.

What are the payment methods for USDC?

You can acquire USDC through several direct channels, including debit or credit cards, bank transfers, Apple Pay, Google Pay, PayPal, and various regional payment methods. Once purchased, USDC is sent directly to a digital wallet you control. This ensures that no exchange or third party holds your funds, giving you immediate ownership and access to the asset for sending or receiving.

Is USDC remittance faster than traditional bank transfers?

Yes. Traditional international wire transfers often take several days to clear due to intermediary banks and compliance checks. USDC remittances operate on blockchain networks, allowing for near-instant settlement regardless of the time of day or day of the week. This speed is particularly valuable for urgent personal transfers or business payments where cash flow timing is critical.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!