How USDC Remittances Work

Traditional cross-border payments rely on a fragmented network of correspondent banks. When you send money internationally through a bank, the funds often pass through multiple intermediaries, each taking a cut and adding processing time. The result is high fees and settlement delays that can stretch from days to weeks.

USDC remittances cut out this middleman layer. Because USDC is a stablecoin pegged to the US dollar, it moves directly between digital wallets on a blockchain. This direct transfer model means the money doesn't need to bounce between different banking systems to reach its destination. Instead, the transaction settles on-chain, often within minutes, regardless of the time of day or day of the week.

This structural difference is why USDC costs significantly less than traditional wire transfers. Without the need for correspondent banking fees, the primary costs are limited to network gas fees and the service provider's spread. For the sender, this translates to more of the intended amount actually reaching the recipient.

Cost comparison: USDC vs traditional transfers

The headline difference between sending money via USDC and legacy providers is the fee structure. Traditional money transfer operators (MTOs) like Western Union and MoneyGram typically charge a flat fee plus a percentage of the transfer amount, often compounded by unfavorable exchange rate markups. In contrast, USDC-based remittance solutions like BCRemit operate on a network fee model. Because the underlying asset is a stablecoin pegged to the US dollar, the value transfer is direct, eliminating the currency conversion spreads that inflate traditional costs.

According to case studies from Circle, the integration of USDC into remittance rails allows providers to bypass the correspondent banking network. This structural change reduces the friction and cost associated with cross-border settlements. While traditional transfers can cost users 5-7% of the total amount sent, particularly for smaller ticket sizes, USDC solutions often bring this cost down to under 1%, primarily consisting of minimal network gas fees and the provider's service fee.

The table below compares the typical cost, speed, and availability of USDC-based remittances against traditional money transfer services. These figures represent average market conditions for standard remittance corridors.

| Provider | Typical Fee | Settlement Time | Reach |

|---|---|---|---|

| USDC (e.g., BCRemit) | < 1% + network fee | Minutes | Global, 24/7 |

| Wise | 0.4% - 1.5% | 1-2 days | Major corridors |

| Western Union | 5% - 10% | Minutes - Days | Global, physical agents |

| MoneyGram | 5% - 9% | Minutes - Days | Global, physical agents |

While USDC offers a clear cost advantage, it is important to note that traditional providers like Wise have optimized their own fees to remain competitive for larger transfers. However, for smaller, frequent remittances, the percentage-based fees of MTOs make them significantly more expensive. The speed advantage of USDC is also notable; while Wise and traditional banks rely on business days for settlement, USDC transactions settle on-chain in minutes, regardless of weekends or holidays.

Settlement speed and liquidity

The primary advantage of USDC in cross-border transfers is the elimination of correspondent banking delays. Traditional wire transfers often require two to five business days to settle because they must pass through multiple intermediary banks, each performing its own compliance checks and clearing cycles. USDC bypasses this chain entirely. By moving value directly between digital wallets on the blockchain, the transaction finality occurs in seconds, regardless of the distance between sender and receiver.

This speed is not just a convenience; it fundamentally changes how liquidity is managed for remittances. In the traditional system, funds are often "in transit" for days, effectively locking up capital and creating uncertainty for both the sender and the recipient. With USDC, the settlement is immediate. Once the blockchain confirms the transaction, the funds are available. This reduces the window for fraud and eliminates the need for pre-funding accounts in foreign currencies, which ties up working capital.

However, "instant" settlement on the blockchain does not always mean instant availability in the recipient's local bank account. The final step involves a fiat on-ramp, where a service provider converts USDC into local currency and deposits it into the recipient's bank. While the blockchain leg is nearly instantaneous, the fiat settlement can still take time depending on the provider and the local banking infrastructure.

For high-stakes financial decisions, this distinction is critical. If you need funds available for an urgent payment, USDC offers a significant edge over traditional wires, but you must account for the final conversion step. The speed advantage is real, but it is not magic; it is a result of removing the middlemen from the ledger, not from the physical banking system.

Regulatory Risks and Compliance

Stablecoins like USDC operate in a regulatory gray area that can shift overnight. Unlike a central bank digital currency (CBDC), which is a direct liability of the government, USDC is a private token issued by Circle. This distinction matters because it means USDC relies on corporate compliance rather than sovereign backing. If regulators tighten rules on stablecoin issuers, your ability to move money could be restricted, regardless of how fast the blockchain is.

The safety of USDC hinges on its reserve backing. Circle claims that USDC is fully backed by cash and short-dated U.S. Treasuries held in segregated accounts with major financial institutions like The Bank of New York Mellon. BlackRock manages the Treasury portion of these reserves. This structure is designed to ensure that every token has a corresponding dollar in the bank, but it also introduces counterparty risk. If one of these custodians fails or faces legal action, the stability of the peg could be tested.

Investors should review Circle’s monthly attestations to verify that reserves match the circulating supply. These reports are public, but they are not audited in the same rigorous way as traditional bank statements. For cross-border payments, this transparency is a double-edged sword: it builds trust, but it also highlights that the system is vulnerable to regulatory changes in the U.S. and other jurisdictions where Circle operates.

When USDC remittance makes sense

USDC isn't a universal replacement for traditional money transfer operators (MTOs) like Western Union or Wise. It works best for users who already understand digital wallets and need to move larger sums quickly. For most people sending small amounts under $200, the friction of setting up a crypto wallet outweighs the fee savings.

The demographic profile of stablecoin users skews younger and more financially literate. Research from ScienceDirect indicates that stablecoin remittance users tend to be more educated and involved in higher-value transactions. If you are comfortable managing private keys and navigating blockchain explorers, USDC offers near-instant settlement at a fraction of the cost of SWIFT transfers.

However, if you prioritize simplicity and established consumer protections, stick to regulated fiat rails. Traditional banks and licensed MTOs offer dispute resolution and customer support that crypto networks simply do not provide. For high-stakes financial decisions, convenience and recourse often matter more than marginal fee reductions.

Frequently asked questions about USDC

Is USDC owned by the US government?

No. USDC is issued by Circle Internet Group, a private company, and is distinct from a central bank digital currency (CBDC). While it is pegged 1:1 to the US dollar, the US government does not issue or guarantee the token itself. Users should understand that holding USDC involves trusting Circle’s compliance and reserve management rather than federal deposit insurance.

Is it safe to keep money in USDC?

USDC is backed by cash and short-dated US Treasury bills held in segregated accounts with qualified custodians like The Bank of New York Mellon, with reserve management handled by BlackRock. This structure provides transparency through monthly attestations, but it is not a bank deposit. The primary risks are smart contract vulnerabilities, exchange insolvency, or regulatory changes affecting Circle’s ability to maintain the peg.

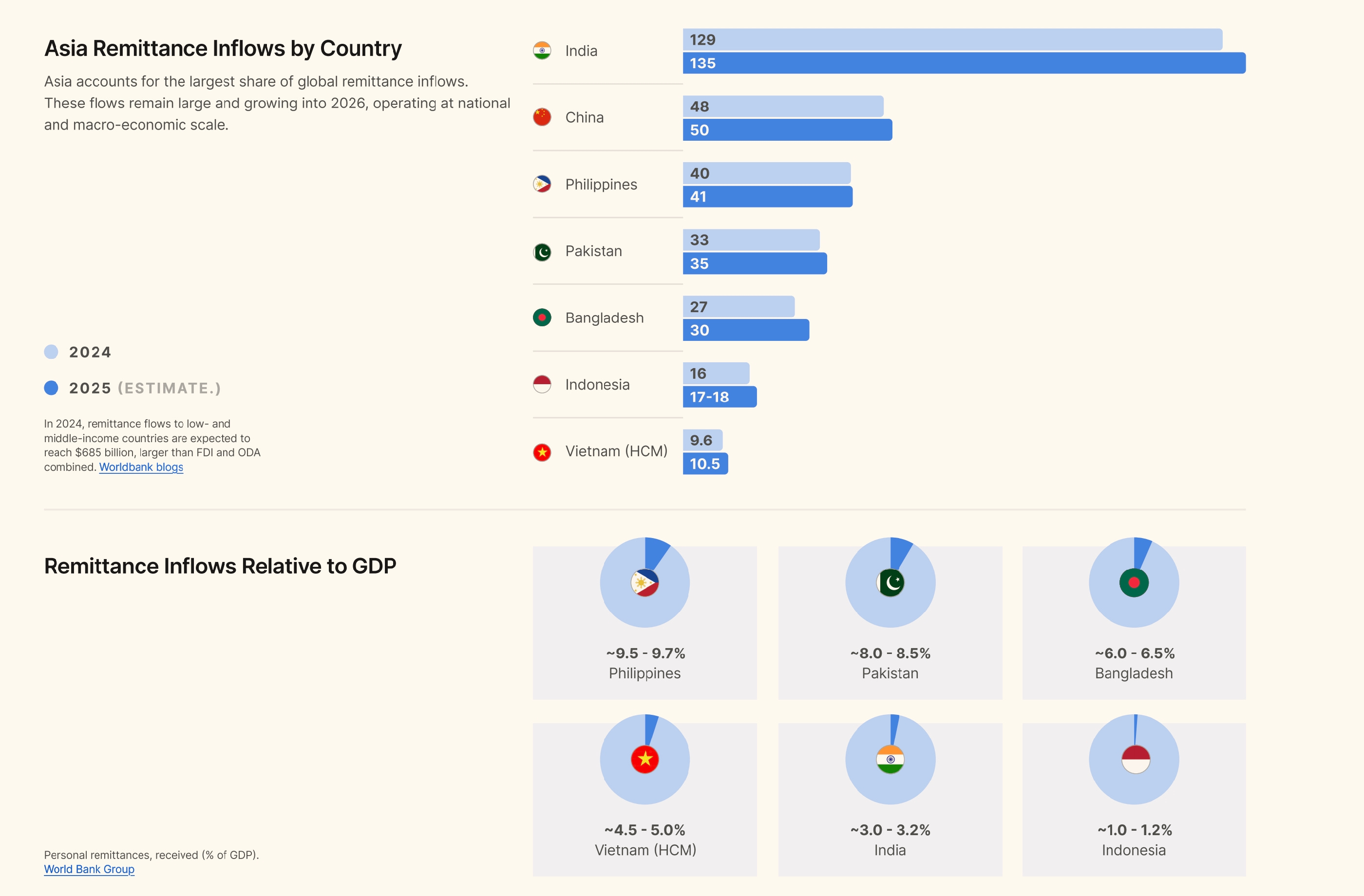

What are the top countries for USDC remittance outflows?

While specific on-chain data for USDC outflows varies by platform, the United States remains the dominant source of global remittances. According to World Bank data, the US sent $79.15 billion in remittances in 2022, followed by Saudi Arabia ($39.35 billion) and Switzerland ($31.91 billion). USDC adoption is highest in corridors where traditional transfer fees are prohibitive, often linking these major outflow nations with high-inflow destinations in Latin America and Asia.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!